Non-documentary condition can be defined as any instruction or condition that is not clearly attributable to a document to be stipulated in a documentary credit. (Gary Collyer, The Guide to Documentary Credits, 3rd Edition, page.157)

Letter of credit has a unique characteristic which is described as a “documentary structure”.

We can see the definition of the “documentary structure” in article 5 of the latest version of the letter of credit rules which is known as UCP 600.

UCP 600 article 5 which is titled “Documents v. Goods, Services or Performance” states that

- “Banks deal with documents and not with goods, services or performance to which the documents may relate.”

UCP 600 article 14 strengthen documentary structure of the letters of credit by stating that

- “A nominated bank acting on its nomination, a confirming bank, if any, and the issuing bank must examine a presentation to determine, on the basis of the documents alone, whether or not the documents appear on their face to constitute a complying presentation.”

As I have explained above banks deal only with the documents in the letters of credit transactions, when determining whether or not a presentation is complying.

This is a very straight forward and easy to understand situation.

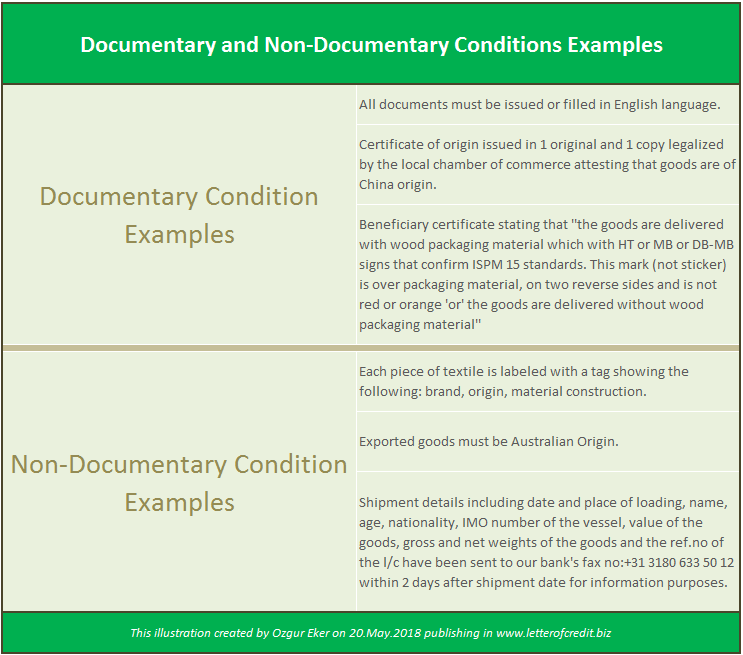

Let me give some examples to the documentary conditions as follows:

- Documentary Condition Example:

All documents must be issued or filled in English language. - Documentary Condition Example:

Certificate of origin issued in 1 original and 1 copy legalized by the local chamber of commerce attesting that goods are of China origin. - Documentary Condition Example:

Beneficiary certificate stating that ”the goods are delivered with wood packaging material which with HT or MB or DB-MB signs that confirm ISPM 15 standards. This mark (not sticker) is over packaging material, on two reverse sides and is not red or orange ‘or’ the goods are delivered without wood packaging material”

Things are getting complicated when a credit requires some conditions to be met, but does not specify a document relating to the condition.

Let me give some examples to the non-documentary conditions as follows:

- Non-Documentary Condition Example:

Each piece of textile is labeled with a tag showing the following: brand, origin, material construction. - Non-Documentary Condition Example:

Exported goods must be Australian Origin. - Non-Documentary Condition Example:

Shipment details including date and place of loading, name, age, nationality, IMO number of the vessel, value of the goods, gross and net weights of the goods and the ref.no of the l/c have been sent to our bank’s fax no:+31 3180 633 50 12 within 2 days after shipment date for information purposes.

If a credit states a non-documentary condition, then things are getting complex not only for exporters or beneficiaries, but issuing and confirming banks as well.

In order to understand the consequences of the non-documentary conditions in a letter of credit transaction we need to have a closer look at the rules and international standard banking practices.

What Does the Letter of Credit Rules Say About the Non-documentary Conditions?

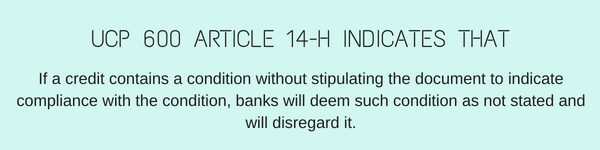

UCP 600 article 14-h indicates that

- “If a credit contains a condition without stipulating the document to indicate compliance with the condition, banks will deem such condition as not stated and will disregard it.”

ISBP 745 paragraph A26 which is titled with “Non‐documentary conditions and conflict of data” further explains the situation and states that

- “When a credit contains a condition without stipulating a document to indicate compliance therewith (“non‐documentary condition”), compliance with such condition need not be evidenced on any stipulated document. However, data contained in a stipulated document are not to be in conflict with the non‐documentary condition. For example, when a credit indicates “packing in wooden cases” without indicating that such data is to appear on any stipulated document, a statement in any stipulated document indicating a different type of packing is considered to be a conflict of data.”

Conclusion:

Issuing banks and applicants should be very careful not to insert any non-documentary conditions to the letter of credit.

They can achieve this by linking each condition to a document.

Beneficiaries should read the credit very well in terms of non-documentary conditions.

If they determine any non-documentary conditions in the credit, they should either have them deleted from the letter of credit or make sure that non-documentary conditions will not be creating a discrepancy during the presentation period.

Remember a data contained in any stipulated document should not to be in conflict with the non‐documentary conditions.

Otherwise banks determine that the presentation is not complying by referring related discrepancies.