Definition of Transshipment: Transhipment means unloading from one means of conveyance and reloading to another means of conveyance during the carriage as enrouted in the letter of credit.

Definition of Partial Shipment: If a beneficiary under a letter of credit ships the credit amount in a single lot, which is corresponding to the whole credit amount, loaded with a single means of conveyance; then this can be defined as a complete shipment.

All other shipments, which are not complete and/or loaded with more than one means of conveyance, can be defined as partial shipments.

What are the Important Points of Transshipment?

Transshipment is not regulated under cash in advance payment, open account or documentary collections rules.

Letter of credit rules have special articles covering transshipments.

Air transportation mostly requires couple of transshipments before the cargo arrives to the airport of destination. Prohibiting transshipment in air transportation may result undesired consequences.

Multimodal transportation must require at least one transhipment. Prohibiting transhipment in multimodal transportation should be avoided.

What are the Important Points of Partial Shipments?

Partial shipment is not regulated under cash in advance payment, open account or documentary collections rules.

Letter of credit rules have special articles covering partial shipments.

Disallowing partial shipments may huge impact on exporter’s shipment flexibility, as a result it must be used very carefully.

If letter of credit amount can not be shipped in a single truck and requires more than one truck usage, partial shipment should not be prohibited when road transportation will be used.

Why Transhipment is not Allowed by Banks?

Transhipment is getting more important for the importers and banks when they are dealing with sanctions, embargoes and trade restrictions. Importers and banks may want to prevent the cargo entering any unwanted country, seaport, airport etc by prohibiting the transshipment.

Other than that the importers may try to prohibit transshipments for their own commercial interests.

Why Partial Shipment is not Allowed by Banks?

Partial shipment will be prohibited by banks mainly on commercial basis. Most of the times the importers request from the issuing banks not to allow partial shipments.

Conclusion:

Both partial shipments and transshipments are important concepts in their own way of effecting the process of letters of credit transactions.

Importers should refrain prohibiting both partial shipments and transshipments as long as legal or commercial conditions dictates so.

On this post, I would like to explain partial shipments in letters of credit.

You can find detailed explanations regarding the definition and conditions of the partial shipments.

Definition: If a beneficiary under a letter of credit ships the credit amount in a single lot, corresponding to the whole credit amount, loaded with a single means of conveyance, then this can be defined as a complete shipment.

All other shipments, which are not complete and/or loaded with more than one means of conveyance, can be defined as partial shipments.

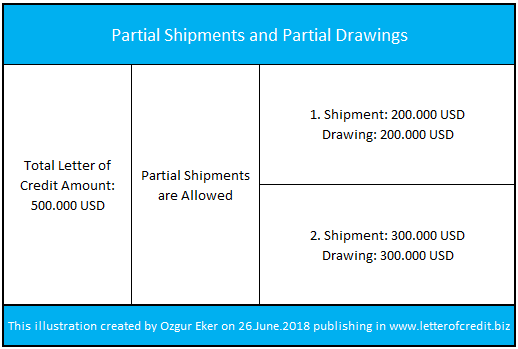

Partial Shipments and Partial Drawings:

If a partial shipment is effected under a letter of credit, then the drawing amount must match the shipped goods.

Partial shipment must correspond to the partial drawing.

Let us assume that a beneficiary makes two partial shipments under a commercial letter of credit. 1st shipment is for the amount of 200.000 USD and 2nd shipment is for the amount of 300.000 USD.

The beneficiary demands 200.000 USD from the issuing bank for the 1st shipment and 300.000 USD for the 2nd shipment.

This mechanism is called partial drawings. Both drawings are independent from each other. For example, 1st drawing may be clean without any discrepancies, but 2nd drawing may be rejected based on a discrepant presentation.

Letter of Credit Example: Partial Shipments and Partial Drawings

What are the Conditions of a Partial Shipment?

In certain situations it would be a very tricky job determining whether a partial shipment has been effected or not.

Things are getting complicated especially if more than one set of transport documents have been presented under the same presentation.

For this reason it would be better to explain partial shipment definitions under two conditions:

Determining partial shipments when only one set of original transport documents have been presented:

It is comparatively straight forward determination of the partial shipment if only one set of original transport documents have been presented and they are evidencing shipment on one means of conveyance within the same mode of transport.

Checking the shipment quantity and drawings would be enough.

If the letter of credit amount has not been drawn in full and documents are showing that the goods have not been loaded completely, you can reach to the conclusion that partial shipment has been effected.

Important Note: Please kindly keep in mind that the letter of credit rules allow some tolerances even when partial shipments are prohibited.

How to determine partial shipment when presentation consisting of one set of transport documents?

Example 1:A letter of credit has been issued in SWIFT format, subject to UCP latest version, with the following details:

Letter of Credit Conditions

Field 43P: Partial Shipments: Not Allowed

Field 43T: Transhipment: Allowed

Field 45A: Description of Goods and or Services: Frozen Seabass and Seabream. Frozen Seabass Price: 6 USD/KGS Frozen Seabream Price: 7USD/KGS Quantity: 5000 KGS seabass and 5000 KGS seabream 10.000 KGS in total. Delivery Terms: CIF Rotterdam Seaport Netherlands Incoterms 2010.

Field 46A: Documents Required:

3 original signed commercial invoices and 3 copies.

Certificate of Origin issued and certified by the Chamber of Commerce in Beneficiary’s country indicating South African origin of the goods.

Insurance certificate or policy in assignable form and endorsed in blank for 110% CIF commercial invoice value covering all risks showing claims payable in Netherlands in commercial invoice currency.

Full set of original bill of lading shipped on board established to the order of Bank Nederlandse Gemeenten notify applicant company marked freight prepaid.

The beneficiary presented one set of original bills of lading among other documents with the following data:

Bill of Lading and Conclusion:

Determining partial shipments when more than one sets of original transport documents have been presented:

If more than one sets of original transport documents have been presented under the same letter of credit presentation, you can not determine whether partial shipment has been effected by simply comparing the actual shipment quantity and amount with the letter of credit quantity and amount.

You have to check couple of additional variables in order to reach the correct conclusion.

How to determine whether partial shipment has been effected when the presentation consisting of more than one sets of transport documents:

Step 1 : Checking the total quantity and amount shipped: If total quantity and amount less than what letter of credit states you can say that partial shipment has been effected.

If actual shipment amount and quality equals to the letter of credit requirements, then you further need to check the transport documents.

Step 2 : Checking the transport documents: If the transport documents evidencing shipment commencing on the same means of conveyance and for the same journey, provided they indicate the same destination, will not be regarded as covering a partial shipment, even if they indicate different dates of shipment or different ports of loading, places of taking in charge or dispatch.

If the transport documents evidencing shipment on more than one means of conveyance within the same mode of transport, this will be regarded as covering a partial shipment, even if the means of conveyance leaves on the same day for the same destination.

Example 2: A letter of credit has been issued in SWIFT format, subject to UCP latest version, with the following details:

Letter of Credit Conditions

Field 43P: Partial Shipments: Not Allowed

Field 43T: Transhipment: Allowed

Field 45A: Description of Goods and or Services: Frozen Sliced Red Peppers and Frozen Sliced Potatoes. Frozen Sliced Red Peppers Price: 2 USD/KGS Frozen Sliced Potatoes Price: 1,5 USD/kgs Quantity: 10000 kgs peppers and 10000 kgs potatoes 20.000 KGS in total. Delivery Terms: CIF Dammam Seaport Kingdom of Saudi Arabia Incoterms 2010.

Field 46A: Documents Required:

3 original signed commercial invoices and 3 copies.

Certificate of Origin issued and certified by the Chamber of Commerce in Beneficiary’s country indicating South African origin of the goods.

Insurance certificate or policy in assignable form and endorsed in blank for 110% CIF commercial invoice value covering all risks showing claims payable in Kingdom of Saudi Arabia in commercial invoice currency.

Full set of original bill of lading shipped on board established to the order of AlAhli Bank notify applicant company marked freight prepaid.

The beneficiary presented two sets of original bills of lading among other documents with the following data:

Conclusion of the Example 2: Letter of credit amount shipped in full. 10000 kgs frozen sliced red peppers and 10000 KGS frozen sliced potatoes have been loaded which makes 20.000kgs in total as the same as letter of credit requested, but presentation consisting of more than one set of bills of lading, which means that we have to look at the bills of lading in order to determine whether partial shipment effected or not.

First bill of lading shows the vessel name “Sea Voyager” voyage number “IV”. Second bill of lading shows the vessel name ” Blue Bird” voyage number “1337 “. There are two means of conveyances (two different vessels) have been utilized on this shipment, as a result partial shipment has been effected.

Under an ordinary letter of credit, the issuing bank demands a full set of clean shipped on board ocean bills of lading from the beneficiary.

But what is a full set of bill of lading according to the letter of credit rules? How does a beneficiary make sure that he presents a full set of bills of lading?

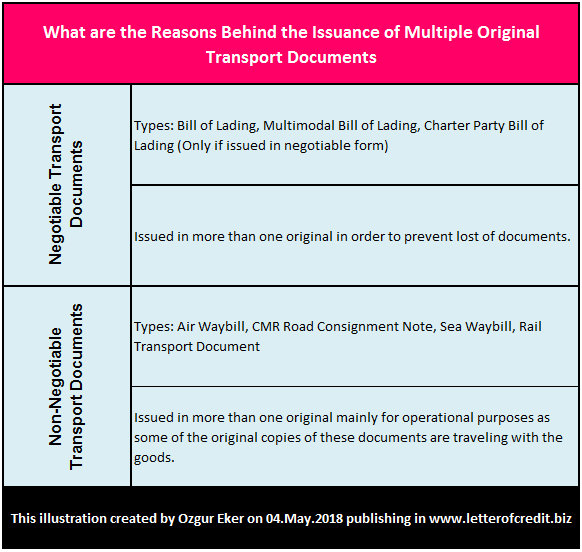

Most of the transport documents, that is subject to international transportation, issued in more than one originals.

For example, a CMR road consignment note is issued in 3 original copies. The first copy for the exporter, the second to accompany the goods; and the third for retention by the carrier. (1)

Understanding the Reasons Behind the Issuance of Multiple Original Transport Documents:

International transport documents can be classified under two main groups: Negotiable transport documents and non-negotiable transport documents.

Negotiable transport document is a title of goods, such as an original bill of lading, which can be transferred to another party by endorsement.

At least one original negotiable transport document must be surrendered to the carrier by the consignee at the place of destination to collect the goods.

Negotiable transport documents are issued in more than one originals in order to prevent lost of documents.

Non-negotiable transport document is a not a title of property and the consignment is placed at the disposal of the stipulated consignee against a proof of identity without further need to surrendering any original transport document.(2)

Non-negotiable transport documents are issued in more than one originals mainly for operational purposes as some of the original copies of these documents are traveling with the goods.

Full Set of Ocean Bills of Lading Under a Letter of Credit

According to the letter of credit rules, a bill of lading is to indicate the number of originals that have been issued and all of the originals stated on the bill of lading have to be presented by the beneficiary to the issuing bank, unless otherwise indicated in the credit.

For example, container carriers issue bills of lading in a set of 3 original and 3 copies as an established tradition for decades.

The letter of credit rules taking into account only the original bills of lading as a transport document by disregarding the non-negotiable copies.

Example:

A letter of credit issued asking for a full set of clean ”shipped on board” negotiable bill of lading showing freight prepaid made out/endorsed to the issuing bank, notifying the issuing bank and the applicant with full address.

The bill of lading indicated that it has issued in 3 originals.

The beneficiary has presented all of the 3 originals as a full set of bills of lading.

Important Note: The beneficiary could have presented 3 originals and 3 copies of the bills of lading without any problem.

Letter of Credit Rules:

UCP 600 – Article 20 – Bill of Lading

iv- Be the sole original bill of lading or, if issued in more than one original, be the full set as indicated on the bill of lading.

ISBP 2007 – Full set of originals Paragraph 93

As per UCP 600 article 20 transport document must indicate the number of originals that have been issued. Transport documents marked “First Original”, “Second Original”, “Third Original”, “Original”, “Duplicate”, “Triplicate”, etc., or similar expressions are all originals. Bills of lading need not be marked “original” to be acceptable as an original bill of lading. In addition to UCP 600 article 17, the ICC Banking Commission Policy Statement, document 470/871(Rev), titled “The determination of an ‘Original’ document in the context of UCP 500 sub-Article 20(b)” is recommended for further guidance on originals and copies and remains valid under UCP 600. The content of the Policy Statement appears in the Appendix of this publication, for reference purposes. (Please keep in mind that ISBP 2007 has been updated and is not the effective version as of July 2013.)

References:

The CMR Convention, The British International Freight Association (BIFA) Website, Retrieved: 21.06.2018

Shipping and Incoterms, Practice Guide, UNDP Practice Series, Page:50

When the addresses of the beneficiary and the applicant appear in any stipulated document, they need not be the same as those stated in the credit or in any other stipulated document, but must be within the same country as the respective addresses mentioned in the credit.

Laura from Germany is asking a question regarding the beneficiary’s address.

She would like to know whether banks can control the address indicated in the letter of credit by comparing it with their internal systems. Below you can find her question and my answer respectively.

Question:

Good day,

I would like to know whether you can advise what responsibility the bank would have if they receive an L/C for their client, to the correct NAME of the beneficiary BUT the address indicated in the L/C does not match with the address in the registry of the bank (customer’s address).

Is the bank supposed to recheck this information BEFORE accepting the L/C?

Also, when the bank receives the shipping documents from their client, again the address in the invoice, packing list, etc. is NOT the same address as they one they have in their registry.

A beneficiary of the letter of credit has to present discrepancy free documents in order to get his payment from the issuing bank.

The issuing bank has to follow the letter of credit rules when checking the documents.

Related article of the letter of credit rules is mentioned below:

Article 14 – Standard for Examination of Documents

j: When the addresses of the beneficiary and the applicant appear in any stipulated document, they need not be the same as those stated in the credit or in any other stipulated document, but must be within the same country as the respective addresses mentioned in the credit. Contact details (telefax, telephone, email and the like) stated as part of the beneficiary’s and the applicant’s address will be disregarded. However, when the address and contact details of the applicant appear as part of the consignee or notify party details on a transport document subject to articles 19, 20, 21, 22, 23, 24 or 25, they must be as stated in the credit.

k. The shipper or consignor of the goods indicated on any document need not be the beneficiary of the credit.

As it is seen from above quotes, neither the address of the beneficiary or the address of the applicant has to match the addresses stated in the letter of credit. Only exception of this rule is the the consignee or notify party details on the transport documents.

Additionally, according to the letter of credit rules the shipper or consignor of the goods indicated on any document need not be the beneficiary of the credit.

Which means that 3rd party documents are acceptable.

But in some situations, the issuing bank do not allow presentation of 3rd party documents by adding special conditions to the letter of credit.

As a result it is advisable to use both beneficiary and applicant names on the documents as stated in the letter of credit.

Also try to copy the correct addresses of the beneficiary and the applicant to the documents from the letter of credit without making any mistake.

There is no ground for a bank to check a beneficiary’s address with his internal system, as long as the letter of credit do not indicate so.

I assume the issuing bank may have suspected from a fraudulent transaction.

Modes of Transport is a term used to distinguish substantially different ways to perform transport.

The most frequently used modes of transport in international trade are air transportation, land transportation, rail transportation, sea transportation and multimodal transportation.

Means of Conveyance is a term describing something that serves as a means of transportation, such as a vessel, truck, aircraft etc.

On this page, I will try to explain two important logistics terms: modes of transport and means of conveyance and their applications under the letter of credit rules.

Modes of Transport in Letters of Credit:

Modes of transport term used in connection with the determination of the multimodal transport documents under the letter of credit transactions.

Multimodal transportation is the movement of one unit load from origin to destination by several modes of transportation under one document without breaking up the unit load. (1)

According to the letter of credit rules, if a transport document covers at least two different modes of transport, then it is regarded as a multimodal bill of lading.

The title of the transport document is not important.

UCP 600 Article 19 – Transport Document Covering at Least Two Different Modes of Transport

a. A transport document covering at least two different modes of transport (multimodal or combined transport

document), however named,…

Example: A letter of credit asks for a full set of shipped on board multimodal ocean bills of lading marked freight payable at destination made out to the order of issuing bank marked notify applicant.

Transport Document: The bill of lading shows port to port sea shipment between a German port to Djibouti Port and a land or rail transport between Djibouti Port to Modjo Dry Port. The presented document is a multimodal bill of lading according to the letter of credit rules, regardless of the title of the transport document.

Means of Conveyance in Letters of Credit:

Means of conveyance term used in connection with the determination of the transshipment and partial shipments under the letter of credit transactions.

Transshipment:

According to the letter of credit rules transhipment means unloading from one means of conveyance and reloading to another means of conveyance (whether or not in different modes of transport) during the carriage that takes place between the route indicated in the credit.

For example, under sea shipments transhipment means unloading from one vessel and reloading to another vessel during the carriage from the port of loading to the port of discharge stated in the credit.

According to the letter of credit rules transhipment can be occurred only if,

happened during the carriage that takes place between the route indicated in the credit.

cargo is unloading from one means of conveyance and reloading to another means of conveyance (whether or not in different modes of transport).

Partial Shipments:

According to the letter of credit rules, a presentation consisting of one or more sets of transport documents evidencing shipment on more than one means of conveyance within the same mode of transport will be regarded as covering a partial shipment, even if

the means of conveyance leave on the same day for the same destination.

References:

Shipping and Incoterms, Practice Guide, UNDP Practice Series, Page: 6

According to the letter of credit rules, the beneficiary should communicate its acceptance of the amendment to the bank that advised such amendment.

The beneficiary should give notification of acceptance or notification of rejection of an amendment.

If the beneficiary fails to give such notification of acceptance, a presentation that complies with the credit and to any not yet accepted amendment will be deemed to be notification of acceptance by the beneficiary of such amendment.

As of that moment the credit will be amended.

But, what happens if a beneficiary of a letter of credit partially accepts an amendment?

Real Life Example: Kuldeep is Asking This Question From India

Question: We have opened a confirmed 100% irrevocable lc at sight to our supplier in China on 28.January.2014 from our local bank in India.

Just after the issuance of the letter of credit our supplier contacted us for demanding more shipment period.

We amend the letter of credit by extending the latest date of shipment and expiry date.

One month later, our supplier, who is the beneficiary of the commercial letter of credit, got in touch with us again and requested another extension of the shipment period. We agreed and amended the letter of credit second time.

However the exporter again demanded from us more time to shipment. This time we add additional conditions to our amendment in addition to extension of latest date of shipment and date of expiry of the credit.

The seller accepted some clauses in the 3rd amendment and rejected others.

We have warned our supplier that partial acceptance of amendments is not allowed according to the UCP 600.

We told him that partial acceptance of amendments means the rejection of that particular amendment altogether. Our supplier denied our requests and insisted on his stance.

What we would like to know is that whether our letter of credit expired or not? You can find latest date of shipment dates and expiry dates corresponding to our amendments on above figure.

Answer: Partial acceptance of an amendment is not allowed and will be deemed to be notification of rejection of the amendment.

The beneficiary neither accepted the 3rd amendment nor they have made any shipment before the latest date of shipment or presented the documents before the expiry date.

Letter of credit is an irrevocable and conditional payment obligation of the issuing bank.

As the letter of credit is irrevocable, its terms and conditions can not be changed without the consent of the beneficiary.

The beneficiary may find some of the terms and conditions of the credit unacceptable. Under such circumstances, the beneficiary has three options,

leaving the deal by not utilizing the letter of credit

making shipments with the original letter of credit by taking discrepancy risk

seeking an amendment by applying to the applicant.

Amendment in a letter of credit, a change in terms and conditions of the letter (e.g., extension of the letter of credit´s validity period, shipment deadline, etc.) usually to meet the needs of the seller. (1)

But what is the effectiveness date of an amendment?

The question comes from Vincent, who is asking a question regarding the effectiveness date of an amendment.

Here is his question as arrived by e-mail.

If the bank issues an amendment directly to the beneficiary decreasing the letter of credit amount without indicating an effective date for the amendment, is the decrease effective the date the amendment is issued or is the decrease effective the date the beneficiary agrees to the amendment.

What is your opinion, with of course no responsibility for providing such an opinion.

Regards

Vincent

Dear Vincent ,

In order to find the right answer to your question we need to look at the related part of the letter of credit rules.

Amendments are explained at article 10 in UCP 600.

UCP 600 states that “a credit can neither be amended nor cancelled without the agreement of the issuing bank, the confirming bank, if any, and the beneficiary.”

UCP 600 article 10 continues to clarify effectiveness date of an amendment for the issuing bank and the confirming bank as follows “an issuing bank is irrevocably bound by an amendment as of the time it issues the amendment.

A confirming bank may extend its confirmation to an amendment and will be irrevocably bound as of the time it advises the amendment.”

On the next couple of phrases explains the position of a beneficiary against amendments.

“The terms and conditions of the original credit (or a credit incorporating previously accepted amendments) will remain in force for the beneficiary until the beneficiary communicates its acceptance of the amendment to the bank that advised such amendment.”

As UCP 600 clearly indicates letter of credit will remain in force as is for the beneficiary until the beneficiary communicates its acceptance of the amendment.

But how beneficiaries can communicate their acceptance to amendments. This would be a good discussion topic for a future page.

A clean transport document or a “clean on board” clause relates to the condition of the goods and/or packaging.

If, on receipt of the goods, the carrier finds that the packaging or the goods are defective, he will make a notation on the transport document to this effect to avoid being subsequently held responsible for such defect.

Hence, the document is no longer clean, and any objections or claims for damages will have to be directed to the consignor. (1)

If the word “clean” appears on a bill of lading and subsequently it has been deleted, the bill of lading will not be deemed to be claused or unclean unless it specifically bears a clause or notation declaring that the goods or packaging are defective.

Clauses or notations on the bills of lading, which expressly declare a defective condition of the goods or packaging are not acceptable by the letter of credit rules.

Clauses or notations which do not expressly declare a defective condition of the goods or packaging (e.g., “packaging may not be sufficient for the sea journey”) do not constitute a discrepancy.

However, a statement on the transport document declaring that the packaging “is not sufficient for the sea journey” would not be acceptable.

One of my reader is asking below question from Belgium. She is director of a shipping company. She would like to know more about clean on board notations on bills of lading.

We have a persistent shipper who insists to have the word ‘clean’ added before shipped on board in their B/Ls. Have tried to explain that a B/L without clauses/remarks is a clean B/L. Can you refer to a certain part on your website where I can find official explication to convince them ?

Thanks in advance.

director of XYZ Shipping Company

Dear Director,

I can suggest you to inform below UCP 600 article to your shipper.

UCP 600 – Article 27

Clean Transport Document

A bank will only accept a clean transport document. A clean transport document is one bearing no clause or notation expressly declaring a defective condition of the goods or their packaging. The word “clean” need not appear on a transport document, even if a credit has a requirement for that transport document to be “clean on board”.

UCP 600 defines below documents as transport documents :

Transport Document Covering at Least Two Different Modes of Transport

Bill of Lading

Non-Negotiable Sea Waybill

Charter Party Bill of Lading

Air Transport Document

Road, Rail or Inland Waterway Transport Documents

Courier Receipt, Post Receipt or Certificate of Posting

References:

Documentary credits in practice, Reinhard Längerich, Second edition – 2009, Published by: Nordea, Page: 146

Shipping and Incoterms, Practice Guide, UNDP Practice Series, Page:12

If issuing bank determines that the presentation is complying then the issuing bank must honor. If credit is available by sight payment you should expect to receive your funds within couple of days after the end of the document evaluation period, which is 5 banking days.

Malik from Pakistan is asking a question regarding the responsibilities of the banks against presentations of documents. Below you can find his question.

Dear Sir,

I request you to please answer the following questions for my better understanding, and also please give example if possible.

In how many days Import L/C opening bank should send the payment or discrepancies to beneficiary of Sight L/C. Some persons saying 3 days and some saying 5 days, which one is correct under UCP 600.

Dear Malik,

A nominated bank, a confirming bank and the issuing bank must determine whether presentation is complying or not maximum five banking days following the day of presentation.

This is governed under UCP 600 article 14-b as follows:

“A nominated bank acting on its nomination, a confirming bank, if any, and the issuing bank shall each have a maximum of five banking days following the day of presentation to determine if a presentation is complying.”

There are two options available for the banks after they receive a presentation:

Option 1 : Determining a non-complying presentation

Option 2 : Determining a complying presentation

Non-Complying Presentation:

If issuing bank determines that the presentation is not complying then issuing bank may refuse to honor.

The issuing bank decides to refuse to honor, it must give a single notice to that effect to the presenter, in other terms to the beneficiary.

Once the issuing bank sends its single notice to the beneficiary within a maximum of five banking days period following the day of presentation, then its responsibility will be ended to the beneficiary under a non-complying presentation in terms of UCP 600 rules.

Complying Presentation:

If issuing bank determines that the presentation is complying, then the issuing bank must honor.

If credit is available by sight payment, you should expect to receive your funds within couple of days after the end of the 5 banking day period.

Reimbursement is defined as a compensation paid to someone for an expense.

In order to be reimbursed by another person or organisation, first of all you have to make some expenses, then you will be qualified for a reimbursement.

The same logic apply to the reimbursement as a trade finance term.

A confirming bank or a nominated bank first honors or negotiates against a complying presentation under a letter of credit and then they will be reimbursed by the reimbursing banks in accordance with the issuing banks authorization.

Reimbursing Bank:

Reimbursing bank is the bank that, at the request of the issuing bank, is authorized to pay, or accept and pay time draft under a documentary credit in accordance with UCP 600 article 13 or if incorporated, the ICC uniform Rules for Bank-to-Bank Reimbursements under Documentary Credits (URR 725). (1)

What is the Function of a Reimbursing Bank Under a Letter of Credit?

There are two possible reasons that makes a reimbursing bank necessary under a documentary credit transaction.

First reason may be that the confirming bank does not trust the issuing bank in terms of risk issues and demands more security. In this situation presence of the reimbursing bank is a requirement for the confirmation.

Without receiving a reimbursement undertaking from the reimbursing bank, the confirming bank may elect not to add its confirmation to the credit.

Note: Please keep in mind that confirmation process is a commercial decision and no bank is forced to add its confirmation to any letter of credit. Please read my article Confirmation and Confirmed Letter of Credit for more detail.

Second reason could be that the issuing bank and nominated bank (in case confirmed letter of credit confirming bank) do not have an account relationship, as a result they may be requiring a third bank’s service for the settlement.

What are the Rules Covering Bank-to-Bank Reimbursements Under Letters of Credit?

There are two options for the reimbursement rules.

Reimbursements must be governed either by URR 725 or UCP 600 article 13 for the letters of credit which are opened according to latest documentary credit rules.

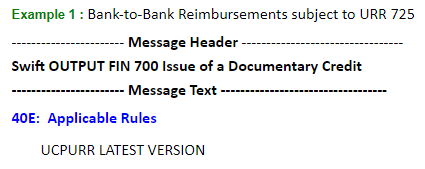

URR 725 – The Uniform Rules for Bank-to-Bank Reimbursements under Documentary Credits – ICC Publication No. 725: This is a small size booklet published by ICC that specifically governs the bank-to-bank reimbursements. If issuing bank would like to be the reimbursement is subject to URR 725, then it must make a reference at the swift message when issuing a letter of credit.

Issuing bank put a reference to MT700 swift message under field “40E- Applicable Rules” as “UCPURR LATEST VERSION” which means that letter of credit is subject to latest version of letter of credit rules (UCP 600) and latest version of bank-to-bank reimbursements rules (URR 725).

Note: Additionally the reimbursement authorization should expressly indicate that it is subject to URR 725 – The Uniform Rules for Bank-to-Bank Reimbursements under Documentary Credits.

UCP 600 Article 13: If a credit does not state that reimbursement is subject to the ICC rules for bank-to-bank reimbursements, the UCP 600 article 13 applies.

Some important definitions from URR 725 – The Uniform Rules for Bank-to-Bank Reimbursements under Documentary Credits:

“Claiming bank” means a bank that honours or negotiates a credit and presents a reimbursement claim to the reimbursing bank. “Claiming bank” includes a bank authorized to present a reimbursement claim to the reimbursing bank on behalf of the bank that honours or negotiates.

“Issuing bank” means the bank that has issued a credit and the reimbursement authorization under that credit.

“Reimbursing bank” means the bank instructed or authorized to provide reimbursement pursuant to a reimbursement authorization issued by the issuing bank

“Reimbursement Authorization” means an instruction or authorization, independent of the credit, issued by an issuing bank to a reimbursing bank to reimburse a claiming bank or, if so requested by the issuing bank, to accept and pay a time draft drawn on the reimbursing bank.

“Reimbursement Undertaking” means a separate irrevocable undertaking of the reimbursing bank, issued upon the authorization or request of the issuing bank, to the claiming bank named in the reimbursement authorization, to honour that bank’s reimbursement claim, provided the terms and conditions of the reimbursement undertaking have been complied with.

“Reimbursement Claim” means a request for reimbursement from the claiming bank to the reimbursing bank.

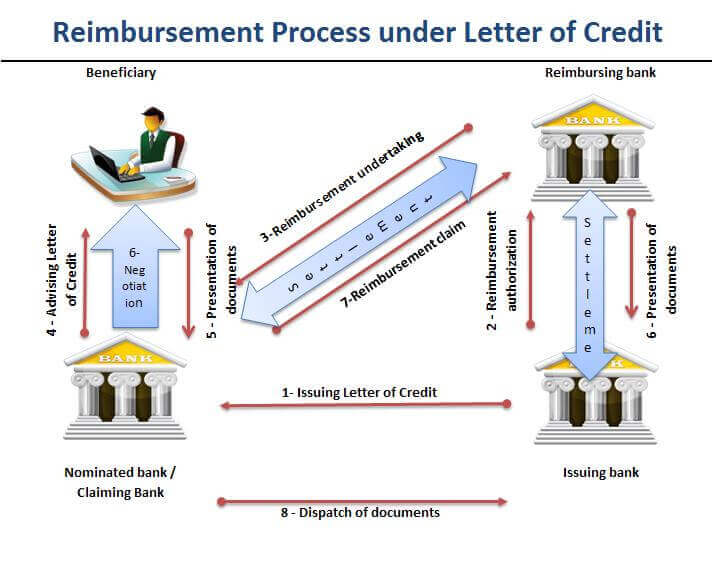

Reimbursement Transaction Under a Letter of Credit:

Issuing bank issues the letter of credit and transmits it to the nominated bank via swift message.

Issuing bank gives reimbursement authorization to reimbursing bank.

Reimbursing bank issues its reimbursement undertaking and transmits it to the nominated bank via swift message.

Nominated bank advices the letter of credit to the beneficiary. (please keep in mind that step 3 and step 4 may be change their sequence)

Beneficiary presents documents to the nominated bank.

Nominated bank checks the documents and negotiate upon a complying presentation.

Nominated bank sends it reimbursement claim to the reimbursing bank. Reimbursing bank reimburse nominated bank according to terms and conditions of the reimbursement undertaking.

Nominated bank send documents to the issuing bank.

On the final stage issuing bank and reimbursing bank arrange settlement between themselves. Issuing bank gets the letter of credit amount from the applicant and releases original shipment documents.

References:

The Guide to Documentary Credits” written by Garry Collyer, 3rd Edition, Page : 36)