Confirmed L/C at sight covers two definitions: Confirmed letter of credit which is payable at sight.

Letters of credit can permit the beneficiary to be paid immediately upon presentation of specified documents (at sight letter of credit), or at a future date as established in the sales contract (term/usance letter of credit). (1)

Confirmation means “a definite undertaking of the confirming bank , in addition to that of the issuing bank, to honour or negotiate a complying presentation” according to latest UCP rules.

By reading this post, you should understand the responsibilities of confirming banks, benefits of confirmed at sight letters of credit and why in some situations at sight confirmed letters of credit mechanism does not work.

Definition of at Sight Letter of Credit:

Latest letter of credit rules, UCP 600, defines four availability options;

A credit must state whether it is available by sight payment, deferred payment, acceptance or negotiation (UCP 600 – Article 6- b).

At sight payment is one of the payment terms in a letter of credit transaction.

At sight letter of credit can be defined as a letter of credit that is payable as soon as the complying documents have been presented to the issuing bank or the confirming bank.

Definition of the Confirmation:

According to latest UCP rules confirmation means,

“a definite undertaking of the confirming bank , in addition to that of the issuing bank, to honour or negotiate a complying presentation”

Confirming Banks’ Responsibilities:

UCP 600 define confirming banks’ responsibilities as follows,

Article 8 – Confirming Bank Undertaking

a. Provided that the stipulated documents are presented to the confirming bank or to any other nominated bank and that they constitute a complying presentation, the confirming bank must:

i. honour, if the credit is available by

a. sight payment, deferred payment or acceptance with the confirming bank;

b. sight payment with another nominated bank and that nominated bank does not pay;

c. deferred payment with another nominated bank and that nominated bank does not incur its deferred payment undertaking or, having incurred its deferred payment undertaking, does not pay at maturity;

d. acceptance with another nominated bank and that nominated bank does not accept a draft drawn on it or, having accepted a draft drawn on it, does not pay at maturity;

e. negotiation with another nominated bank and that nominated bank does not negotiate.

ii. negotiate, without recourse, if the credit is available by negotiation with the confirming bank.

b. A confirming bank is irrevocably bound to honour or negotiate as of the time it adds its confirmation to the credit.

c. A confirming bank undertakes to reimburse another nominated bank that has honoured or negotiated a complying presentation and forwarded the documents to the confirming bank. Reimbursement for the amount of a complying presentation under a credit available by acceptance or deferred payment is due at maturity, whether or not another nominated bank prepaid or purchased before maturity. A confirming bank’s undertaking to reimburse

another nominated bank is independent of the confirming bank’s undertaking to the beneficiary.

d. If a bank is authorized or requested by the issuing bank to confirm a credit but is not prepared to do so, it must inform the issuing bank without delay and may advise the credit without confirmation.

Benefits of At Sight Confirmed Letter of Credit?

Why exporters pay additional fees to have their L/Cs confirmed?

First reason is that the exporters would like to eliminate default risk of the issuing bank.

Second reason is that they would like to receive their payment sooner by removing the issuing bank out of the equation.

Why in some Situations At Sight Confirmed Letter of Credit Mechanism Does not Work?

The nominated banks, whom added their confirmations and became the confirming banks, keep sending documents to the issuing banks and wait for reimbursement even under confirmed at sight letters of credit.

Unfortunately even the confirmation couldn’t eliminate typical nominated bank action: wait for reimbursement, then pay to the beneficiary!

Confirming banks should pay the credit amount against confirming documents to the beneficiaries under at sight letters of credit as letter of credit rules dictate.

But in practice they are ready to act in this way only if they have determined that the issuing bank is defaulted.

Sources:

Documentary Letters of Credit: A Practical Guide, Scotiabank International Trade Services, Page:2

Letter of credit that carries a provision (traditionally written or typed in red ink) which allows a seller to draw up to a fixed sum from the issuing bank, in advance of the shipment can be defined as a red clause letter of credit.

Red clause letters of credit supply advance payments to the exporters before they actually ship the goods to the importers.

Exporters receive advance payments under red clause letters of credit mostly from the issuing banks inside the letters of credit.

It is also possible that the advance payments are payable outside of the letters of credit from the importers to the exporters.

Normally, the issuing banks make the advance payment under red clause letters of credit against presentation of advance payment guarantees issued by the bankers of the exporters, guaranteeing a refund in the event of failure to ship under the credit.

———————————– Instance Type and Transmission —————————-

Original received from SWIFT

Priority/Delivery : Normal

Message Output Reference : 1225 121016XXXXXXXXX5657939061

Correspondent Input Reference : 1225 121016XXXXXXXXX1178375172

—————————————- Message Header —————————————–

Swift OUTPUT FIN 700 Issue of a Documentary Credit

Sender : ASIATRISXXX

Receiver : PCBCCNBJXXX

————————— Message Text ———————————- 27: Sequence of Total

1/1

40A: Form of Documentary Credit

IRREVOCABLE

20: Documentary Credit Number

ASIAIM00004050

31C: Date of Issue

130722

40E: Applicable Rules

UCP LATEST VERSION

31D: Date and Place of Expiry

131230-TURKEY

50: Applicant

ASIA BANK OF TURKEY TAS

BUYUK HAN MAH. ISMAIL HAKKI BEY

CAD. NO:20 34500

SISLI,ISTANBUL/TURKEY

59: Beneficiary – Name & Address

NINGBO PLASTIC MACHINERY CO., LTD.

PLS SEE FIELD 47A ITEM 7 FOR ADDRESS DETAILS

32B: Currency Code, Amount

Currency : USD (US DOLLAR)

Amount : #327.000,00#

39B: Maximum Credit Amount

NOT EXCEEDING

41A: Available With…By… – BIC

ASIATRISXXX

ASIA BANK OF TURKEY TAS BUYUK HAN MAH. ISMAIL HAKKI BEY CAD. NO:20 34500

SISLI,ISTANBUL/TURKEY

BY MIXED PYMT

43P: Partial Shipments

NOT ALLOWED

43T: Transhipment

ALLOWED

44E: Port of Loading/Airport of Departure

ANY CHINESE PORT

44F: Port of Discharge/Airport of Destination

HAYDARPASA PORT ISTANBUL

44C: Latest Date of Shipment

131209

45A: Description of Goods &/or Services

NEW PLASTIC CUP MAKING LINE QTY:1 SET U/P: USD 327.000 FOR TOTAL AMOUNT: USD 327.000,00 AS PER BENEFICIARY’S PROFORMA INVOICE REF NO: NB130522 DD:04.07.2013

INCOTERMS 2010: CIF HAYDARPASA ISTANBUL TURKEY

46A: Documents Required

DULY SIGNED COMMERCIAL INVOICE IN 2 ORIGINALS AND 3 COPIES CERTIFYING IN STRICT CONFORMITY WITH THE BENEFICIARY’S PROFORMA INVOICE REF NO: LL130522 DD:04.07.2013 AND SHOWING QUANTITY, DESCRIPTION , ALSO STATING FOB VALUE OF THE GOODS FREIGHT AND INSURANCE SEPARATELY.

CLEAN ON BOARD B/L IN 3/3 ORGS. AND 3 N/N COPIES ISSUED TO THE ORDER OF ISSUING BANK NOTIFY APPLICANT,MARKED: ‘FREIGHT PREPAID’.

PACKING LIST IN 2 ORG.S AND 2 COPIES.

BENEFICIARY’S CERTIFICATE 1 ORG. STATING THAT SHIPMENT DETAILS INCLUDING DATE AND PLACE OF LOADING,NAME AGE,NATIONALITY,IMO NUMBER OF THE VESSEL,VALUE OF THE GOODS, GROSS AND NET WEIGHTS OF THE GOODS AND THE REF.NO OF THE L/C HAVE BEEN SENT TO OUR BANK’S FAX NO:+90 212 600 50 10 WITHIN 2 DAYS AFTER SHIPMENT DATE FOR INFORMATION PURPOSES.(FAX REPORT AND SHIPMENT DETAILS HAVE BEEN ATTACHED TO THIS DOC.)

CERTIFICATE BY BENEFICIARY STATING THAT ‘CE’MARK HAS BEEN LABELLED ON PACKAGES OF THE GOODS AND TECHNICAL DOCUMENTS IN STRICT CONFORMITY CONCERNING LEGISLATION

FULL SET INSURANCE POLICY ISSUED TO THE ORDER OF ISSUING BANK FOR FULL CIF VALUE PLUS 10 PERCENT AND STATING THE NAME, PHONE AND FAX NUMBERS OF A CLAIMS SETTLING AGENT IN TURKIYE AND CLAIMS PAYABLE IN TURKIYE COVERING THE FOLLOWING RISKS FROM WAREHOUSE TO WAREHOUSE:

+INSTITUTE CARGO CLAUSES (A)

+INSTITUTE WAR CLAUSES (CARGO)

+INSTITUTE STRIKE CLAUSES (CARGO)

+RIOTS AND CIVIL COMMOTIONS,

ALSO INSURANCE TO CERTIFY THAT COVER IS NOT SUBJECT TO A FRANCHISE OR AN EXCESS (DEDUCTIBLE).

CERTIFICATE OF ORIGIN IN 1 ORG. AND 1 COPY LEGALIZED BY THE LOCAL CHAMBER OF COMMERCE ATTESTING THAT GOODS ARE CHINA ORIGIN.

47A: Additional Conditions

ALL DOCUMENTS MUST BEAR OUR L/C REF.

IN CASE OF PRESENTATION OF THE DOCUMENTS WITH DISCREPANCIES, USD 100,00 WILL BE DEDUCTED FROM THE PROCEEDS AS AN ADDITIONAL PROCESS FEE.

DOCUMENTS ISSUED BEFORE L/C OPENING DATE NOT ACCEPTABLE.

PAYMENTS TO BENEFICIARY UNDER RESERVE AND ANY KIND OF GUARANTEE ARE NOT ACCEPTABLE

ALL DOCS MUST BE ISSUED OR FILLED IN ENGLISH

BENEFICIARY’S ADDRESS: DEVELOPED AREA OF NINGBO ECONOMIC DEVELOPMENT ZONE NINGBO CITY CHINA

71B: Charges

ALL BANKING CHARGES AND COMMISSIONS OUTSIDE OF TURKEY ARE FOR BENEFICIARY’S ACCOUNT.

48: Period for Presentation

21 DAYS AFTER SHIPMENT DATE BUT WITHIN CREDIT VALIDITY.

49: Confirmation Instructions

WITHOUT

78: Instruction to Paying/Accepting/Negotiating Bank

30 PCT OF L/C AMOUNT SHALL BE PAID IN ADVANCE UPON RECEIVING ADVANCE PAYMENT GUARANTEE,

70 PCT OF L/C AMOUNT SHALL BE PAID UPON RECEIPT OF CREDIT CONFORM DOCS.

PLS ADVISE US THE REMITTANCE OF THE DOCS. BY MT 754 MSG. QUOTING OUR REF.

72: Sender To Receiver Information

PLS SEND THE DOCS TO FOLLOWING ADDRESS BY DHL IN ONE LOT: ASIA BANK OF TURKEY TAS BUYUK HAN MAH. ISMAIL HAKKI BEY CAD. NO:20 34500 SISLI,ISTANBUL/TURKEY

———————– Message Trailer ——————————

{MAC: 00000000}

{CHK: XXXXXXXX}

According to the current letters of credit rules, UCP 600, credits must state how they are available to beneficiaries in terms of payment type.

UCP 600 – Article 6-b states that “A credit must state whether it is available by sight payment, deferred payment, acceptance or negotiation.”

On this article we explain letters of credit issued available by at sight payment.

Definition:

At sight payment is a payment due on demand. At sight letter of credit can be defined as a letter of credit that is payable as soon as the complying documents have been presented to the issuing bank or the confirming bank.

Payment Time:

When should the beneficiary expect to receive the payment from the issuing bank or the confirming bank under an at sight letter of credit?

If is the issuing bank or the confirming bank finds out that the presentation is complying, then they should transmit the funds to the beneficiary at the earliest convenience.

We know that banks have 5 working days to determine whether a presentation is complying or not.

As a result, under a complying presentation where no additional reimbursement time-frame has been defined, the beneficiary should expect to receive the letter of credit amount from the issuing or confirming bank between 7-10 days after documents received by these banks.

Advantages:

In which circumstances at sight letter of credit can be preferred?

At sight letter of credit can be used in situations where the beneficiary needs funds as soon as the shipment is completed.

At sight letters of credit are mostly used in small to medium size transactions where applicant is located in a relatively high risk country.

Risks:

What are the potential risks in at sight letters of credit?

There is no additional risks associated with at sight letters of credit other than ordinary letters of credit possess.

Swift Usage:

At sight letter of credit is shown in a MT700 swift message under field 41a as below,

The URBPO are the Uniform Rules for Bank Payment Obligations ICC publication No. 750.

URBPO were approved by the ICC national committees and entered into force on 1 July 2013.

Bank Payment Obligations (BPO) is a new payment option for international trade finance. It will be located somewhere between an open account and letter of credit.

Banks play a key role on the Bank Payment Obligation transactions.

The ICC has set itself an ambitious goal to introduce an innovative way for trading counterparties to secure and finance their open account trade transactions via their banking partners.

The new instrument called “Uniform Rules for Bank Payment Obligations” (URBPO; also referred to as ICC URBPO or ICC BPO rules) will enable importers and exporters to involve their preferred banking partners in their trade transactions and get flexible risk and financing services.

Based on standardized messaging and advanced transaction matching operated by SWIFT, this new instrument will accelerate the financial supply chain in support of ever accelerating physical supply chains.

What are the Headings of URBPO?

URBPO consists of total 17 articles.

URBPO – Article 1 Scope

URBPO – Article 2 Application

URBPO – Article 3 General Definitions

URBPO – Article 4 Message Definitions

URBPO – Article 5 Interpretations

URBPO – Article 6 Bank Payment Obligations (BPO) vs. Contracts

URBPO – Article 7 Data vs. Documents, Goods, Services or Performance

URBPO – Article 8 Expiry Date and Submission

URBPO – Article 9 Role of an Involved Bank

URBPO – Article 10 Undertaking of an Obligor Bank

URBPO – Article 11 Amendments

URBPO – Article 12 Charges

URBPO – Article 13 Disclaimer on Effectiveness of Data

URBPO – Article 14 Force Majeure

URBPO – Article 15 Unavailability of a Transaction Matching Application

URBPO – Article 16 Applicable

URBPO – Article 17 Assignment and Transfer

How URBPO 750 Can be Applied to the Bank Payment Obligations ?

The BPO is an irrevocable undertaking given by a bank to another bank that payment will be made on a specified date after successful electronic matching of data according to an industry-wide set of ICC rules known as Uniform Rules for Bank Payment Obligations (URBPO 750).

Match report will be generated by SWIFT’s Trade Services Utility (TSU) or any equivalent transaction matching application.

One of the key features of the BPO is that it supports interoperability between participating banks, because it makes use of a standard set of ISO 20022 messages.

Some important definitions from URBPO 750:

“Obligor bank” means buyer’s bank under Bank Payment Obligations. Obligor bank issues the legally binding, valid, irrevocable but conditional and enforceable payment undertaking to Recipient Bank. Obligor bank is an equivalent term of issuing bank under letters of credit definitions.

“Recipient Bank” means seller’s bank under Bank Payment Obligations.

“Trade Services Utility” (TSU) means a centralized matching and workflow engine providing timely and accurate comparison of data taken from underlying corporate purchase agreements and related documents, such as commercial invoices, transport and insurance.

Each payment method in international trade has strengths and weaknesses.

For example, open account and cash in advance payments are elementary payment options. They are not only simple, but also inexpensive. However, they inherit high volumes of risks either for the importers or the exporters.

Documentary credits, on the other hand, are relatively secure payment methods, but they are complicated and expensive.

Does international trade finance need another payment method? Can bank payment obligation be the right answer?

Definition of Bank Payment Obligation:

Bank payment obligation (BPO) is an irrevocable undertaking given by an Obligor Bank (typically buyer’s bank) to a Recipient Bank (usually seller’s bank) to pay a specified amount on a agreed date under the condition of successful electronic matching of data according to an industry-wide set of rules adopted by ICC.

Some Important Definitions under Bank Payment Obligation (BPO):

“Obligor bank” means buyer’s bank under Bank Payment Obligations. Obligor bank issues the legally binding, valid, irrevocable but conditional and enforceable payment undertaking to Recipient Bank. Obligor bank is an equivalent term of issuing bank under letters of credit definitions.

“Recipient Bank” means seller’s bank under Bank Payment Obligations.

“Trade Services Utility” (TSU) means a centralized matching and workflow engine providing timely and accurate comparison of data taken from underlying corporate purchase agreements and related documents, such as commercial invoices, transport and insurance.

The URBPO, the Uniform Rules for Bank Payment ObligationsICC publication No. 750, are the rules of Bank Payment Obligation adopted by ICC banking commission.

How Does Bank Payment Obligation Work?

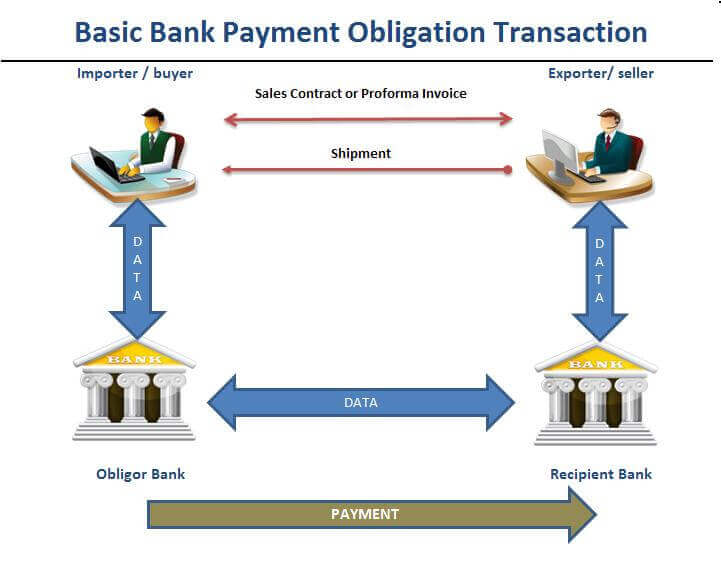

Bank payment obligation and letter of credit have some characteristics in common.

Firstly banks play a key role on both payment methods. Secondly banks are giving the irrevocable payment undertaking.

Figure 1 : Basic Bank Payment Obligation Transaction

Bank Payment Obligation (BPO) has been established on two main expectations,

The use of minimum fields, the buyer, the seller and respective banks agree on the payment terms and conditions and on the minimum trade information required to assess the credit risk;

The dispatch of documents, such as the bill of lading, certificate of origin and certificate of quality, from the seller directly to the buyer.

Given the limited information required by the banks and the accelerated document exchange, companies should expect a lower rate of discrepancies and an acceleration of the settlement process.

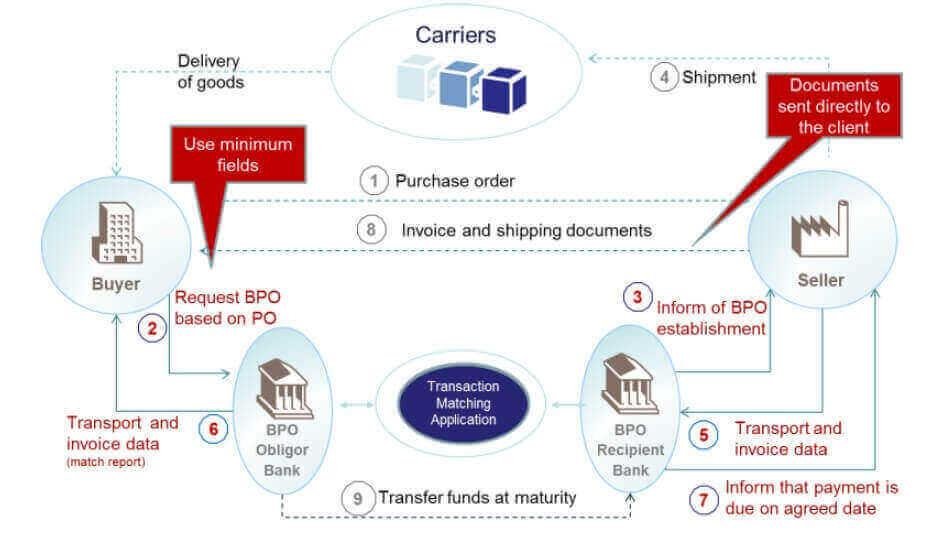

Figure 2 : Bank Payment Obligation Transaction Flow in Detail

Step-by Step Bank Payment Obligation Transaction

Baseline Establishment

Step 1 : Buyer and seller agreed on BPO (bank payment obligation) as a payment term on the sales contract. Buyer send its purchase order to the seller.

Step 2 : Buyer provides the minimum data from the purchase order and conditions of the bank payment obligation to the obligor bank.

Step 3 : Seller confirms the data from the PO and send its acceptance of the BPO conditions to the recipient bank. If both buyer’s and seller’s data are matched on the Transaction Matching Application than the baseline is established. Both buyer and seller will be receiving a matching reports from their banks.

BPO is irrevocable but conditional payment method. (payment is subject to the electronic matching of agreed data-sets)

Matching

Step 4 : Seller ships the goods as agreed on the sales contract.

Step 5 :Seller presents the shipment data and invoice data to its bank, which submits it to Transaction Matching Application for matching.

Step 6 : Buyer receives a match report from its bank. Buyer is invited to accept any mismatches if any.

Step 7 : Seller’s bank inform seller about the successful data-set match.

BPO becomes operative and due according to the agreed payment terms.

Settlement

Step 8 : Seller sends the trade documents directly to the buyer. Buyer will clear goods from the customs with these documents.

Step 9 : On the due date, the obligor bank debits the proceeds from buyer’s account

Bank Payment Obligation Video Presentation

Bank payment obligation (BPO) is the newest payment method in international trade.

Exporters , importers and bank professionals need learning material to understand its usage.

On this page you can find bank payment obligation video presentation. It is prepared by Commerzbank, one of the world’s leading banks in international trade services solutions sector.

What are the Advantages of the BPO (Bank payment Obligation) for the Exporters?

Bank payment obligation is a secure payment method in international trade for the exporters. BPO can be more secure than the letter of credit, because the documents will not be checked by human beings, by which process eliminating alleged discrepancy risks.

The bank payment obligation is cheaper than letter of credit.

Exporters could get their money very fast from the banks under the BPO transactions as documents are checked by an automatic system instantly.

Exporters have more control over the goods until they have been paid by the banks under the BPO transactions as shipment documents will be held by the exporters during the BPO process. Exporters do not send paper documents to the banks. Once exporters receive their money from the banks, they dispatch the documents to the importers separately.

Exporters could reach pre-shipment and post-shipment finance in BPO transactions.

Once the bank payment obligation is opened, it is almost impossible for the importer to cancel the order without the consent of the exporter.

Non-payment risk shifts from importer to importer’s bank, which is called obligor bank in the BPO transaction.

What are the Advantages of the BPO (Bank payment Obligation) for the Importers?

As a payment method the bank payment obligation is more secure than the advance payment, because the BPO is a conditional payment method. Under the BPO transactions, banks send payment amounts to the exporters only after the shipment of the goods, not before.

Issuing a bank payment obligation may prove that the importer is a financially secure and strong company.

The Bank payment obligation is an irrevocable payment method like the letter of credit. As a result importers can convince exporters to make shipments with the BPO much more easily comparing to open account or documentary collections.

The BPO facilitates financing of the shipment for the importers.

It is possible for the importers to pay the transaction amount after receiving the shipment, if a deferred payment has been agreed upon such as “60 days after match”, “90 days after match” etc.

The BPO may protect the buyers, at least in theory, against non-shipments, late shipments and inferior quality of goods shipments.

Bank Payment Obligation – Comparison to Letter of Credit and Open Account

Bank Payment Obligation Comparison to Letter of Credit:

Both bank payment obligation and letter of credit have an irrevocable structure.

Bank payment obligation and letter of credit are governed by ICC rules. BPO rules are URBPO, letters of credit rules are UCPDC.

The conditional payment guarantee is given by a bank to another bank in BPO transactions. BPO is a bank-to-bank payment obligation. The conditional payment guarantee is given by a bank to a commercial company in L/C transactions. (Letters of credit can be issued bank-to-bank transactions as well.)

Letter of credit is paper intensive. BPO is an electronic payment method.

Documents have been checked by banks’ staff manually under letter of credit transactions. Data match completed by online means under BPO transactions.

Under BPO transactions shipment documents would not be sent to the banks.

Letter of credit is slow and expensive. BPO is fast and not as expensive as L/Cs.

Bank Payment Obligation Comparison to Open Account:

Both bank payment obligation and open account are fast and easy to handle.

Open account is the riskiest payment method for the exporters. Nonpayment risk is stemmed from the importer and must be covered by the exporter in full under open account payments. On the contrary, under the BPO the obligor bank is the entity that is giving the payment guarantee to the exporter through the recipient bank. As a result non-payment risk mitigates from the importer to the importer’s bank under BPO transactions.

There are no rules exist for open account payments. On the other hand bank payment obligations can be issued subject to the URBPO 750.

Under open account transactions exporters must finance importers, whereas they can be benefited pre-shipment finance and post-shipment finance under the BPO.

Cash in advance (CIA) is a payment method in international trade. Cash in advance is also known as cash with order or advance payment by most exporters and importers.

Key Characteristics:

One of the main characteristics of a cash in advance payment is that the full order amount will be paid by the importer to the exporter prior to the transfer of ownership of the goods.

In most cases, exporters demand significant advance payments on order confirmation in order to protect themselves against order cancellations. Some common phrases stipulated in sales contracts to this effect are as follows:

%50 of proforma invoice total will be paid on order confirmation, remaining %50 will be paid 1 week before shipment.

%30 of proforma invoice total will be paid 1 week after order confirmation, remaining %70 will be paid against copy of shipment documents send via e-mail or fax.

Cash in advance payment is the most secure payment method in international trade for exporters, because it eliminates non payment risk especially when money transfer is done via wire transfer.

By paying total value of the goods before shipment, importers have to bear some risks such as;

non shipment risks

low quality goods

non compliance risks

custom clearance risks

Cash in Advance Payment Rules:

There is no set of rules exists that governs cash in advance payment used in international trade.

Both UCP 600 and URC 522 is published by ICC (International Chamber of Commerce). On the other hand ICC has not published any rules for the cash in advance payments.

For this reason, exporters and importers have to identify cash in advance payment details on the proforma invoice in order to prevent misunderstandings and possible mistakes.

Payment Settlement Methods for Cash in Advance Payment:

Wire Transfer: Wire transfer is the most secure and preferred cash-in-advance payment settlement method used in international trade transactions.

A wire transfer is an electronic payment service for transferring funds by wire for example, through the Federal Reserve Wire Network or the Clearing House Interbank Payments System (CHIPS). (1)

Wire transfer can either be sent via online banking or traditional banking applications.

In order to complete an international wire transfer correctly you need to specify below details;

Currency of the wire transfer and wire transfer total

Name of the account holder:

Full Name and address of the bank:

Bank Branch:

Account number:

Swift Code: SWIFT is the short form of “Society for Worldwide Interbank Financial Telecommunication”. SWIFT is an industry-owned co-operative supplying secure, standardized messaging services and interface software to nearly 8,100 financial institutions in 207 countries and territories. SWIFT members include banks, broker-dealers and investment managers. While not always required, a SWIFT Code (also known as BIC Code) may be required by some banks for the completion of wire transfers.

IBAN Number: (if applicable) The International Bank Account Number (IBAN) is the international standard for identifying international bank accounts across national borders. The IBAN is comprised of a maximum of 27 alphanumeric characters within Europe and a maximum of 34 outside of Europe (German IBAN: 22 characters). At present, the United States does not participate in IBAN. Therefore, US banks do not have an IBAN number.

Credit Card: For small scale orders credit cards could be used as a viable cash-in-advance payment method in international trade.

As international credit card transactions are typically placed via online, telephone, or fax methods that facilitate fraudulent transactions, proper precautions should be taken to determine the validity of transactions before the goods are shipped.

Although exporters must endure the fees charged by credit card companies, this option may help the business grow because of its convenience.

Payment by Check: Advance payment using an international check may result in a lengthy collection delay of several weeks to months.

Therefore, this method may diminish the original intention of receiving the payment before the shipment.

Moreover, there is always a risk that a check may be returned due to insufficient funds in the buyer’s account.

As a result payment by check is a less-attractive cash-in-advance settlement method in international trade finance.

URC 522 underlines the need for the principal and/or the remitting bank to attach a separate document, the collection instruction, to every collection subject to the Rules.

URC 522 makes it very clear that banks will not examine documents, particularly not to look for instructions.

URC 522 addresses problems banks experience in respect of documents against acceptance (D/A) and documents against payment (D/P)

URC 522 clearly indicates that banks have no obligation to store and insure goods when instructed.

Contents of the URC 522:

A. General Provisions and Definitions

Application of URC 522

Definition of Collection

Parties to a Collection

B. Form and Structure of Collections

Collection Instruction

C. Form of Presentation

Presentation

Sight / Acceptance

Release of Commercial Documents

Documents Against Acceptance (D/A) vs. Documents Against Payment (D/P)

Creation of Documents

D. Liabilities and Responsibilities

Good Faith and Reasonable Care

Documents vs. Goods / Services Performances

Disclaimer for Acts of an Instructed Party

Disclaimer on Documents Received

Disclaimer on Effectiveness of Documents

Disclaimer on Delays, Loss in Transit and Translation

Documentary collection (D/C) is a payment method in international trade.

Documentary collection is also known as Cash Against Documents (CAD) by most exporters and importers.

Documentary collection is more like formal name usually used by bank professionals, whereas cash against documents is a daily life name usually used by importers and exporters.

Key Characteristics:

Importers normally pay for the goods after the shipment in whole. But it is also possible to make an partial advance payment under the documentary collections. For example, it is possible to pay %25 of the transaction amount in advance and %75 is payable via cash against documents (CAD).

Generally, there are two payment options available under the documentary collections: Documents Against Payment (D/P) and Documents Against Acceptance (D/A).

The title of goods belongs to the exporter until the exporter is paid by the importer. But exporter must be very careful about land, rail and air shipments. The transport documents issued under these shipments do not represent the title to the goods.

Although banks play an essential role in documentary collections, they neither check or verify the documents, nor take any risks.

Documentary collections are less complicated than letters of credit. Also documentary collections are less expensive comparing to the letters of credit.

Rules:

Documentary collections are governed by the Uniform Rules for Collections, 1995 Revision, ICC Publication No. 522, shortly known as URC 522.

Documentary collection rules, URC 522, published by International Chamber of Commerce, ICC.

URC 522 will only be effective if it is incorporated into the text of the “collection instruction“.

Collection Instruction and its Scope:

Collection Instruction is a separate document, which the exporter should supply to his bank along with other commercial and financial documents under a documentary collection.

Collection instructions are written in a cover letter format and normally should contain below points.

Governing Rules for the Collection: As an example “This collection is subject to The Uniform Rules for Collections, 1995 Revision, ICC Publication No. 522.”.

Details of the bank from which the collection was received including full name, postal and SWIFT addresses, telex, facsimile numbers and reference.

Details of the principal including full name, postal address, and if applicable telex, telephone and facsimile numbers.

Details of the drawee including full name, postal address, or the domicile at which presentation is to be made and if applicable telex, telephone and facsimile numbers.

Details of the presenting bank, if any, including full name, postal address, and if applicable telex, telephone and facsimile numbers.

Total amount and currency of the documentary collection.

Documents to be supplied: URC 522, the rules of the documentary collections, define two types of documents; financial documents and commercial documents.

Financial Documents : Financial documents means bills of exchange, promissory notes, cheques, or other similar instruments used for obtaining the payment of money.

Commercial Documents: Commercial documents means invoices, transport documents, documents of title or other similar documents, or any other documents whatsoever, not being financial documents

How many number of originals and copies of each document supplied

Conditions for release of documents

Documents Against Payment (D/P): Documents may be released only if the importer makes immediate payment according to the contracted agreement between the exporter and the importer. Also known as sight collection.

Documents Against Acceptance (D/A): Documents may be released only if the importer accepts the accompanying draft, thereby incurring an obligation to pay at a specified future date. In this arrangement the exporter is exposed to the credit risk of the importer and the political risk of the country. Also known as a term collection.

Note: It should be noted that the party preparing the collection instruction should have to clearly define how documents should be handed over to the drawee. If instructing party fails to do so they will be liable for any consequences arising therefrom.

Charges: Charges to be collected, indicating whether they may be waived or not and who is going to pay for charges in detail.

Interest: Collection of interest is a very rare case in documentary collections but if applicable, collection instruction should be indicating whether it may be waived or not, with following information:

a. rate of interest

b. interest period

c. basis of calculation (for example 360 or 365 days in a year) as applicable

Method of payment and form of payment advice.

Instructions in case of non-payment, non-acceptance and/or non-compliance.

Sample Collection Instructions:

Almost every bank has its own collection instructions format available to its clients either in electronic format or hard-copy.

These collection instructions follow the requirements indicated in URC 522, the Uniform Rules for Collections.

Their structure is almost identical. Please click to reach corresponding collection instructions examples provided below.

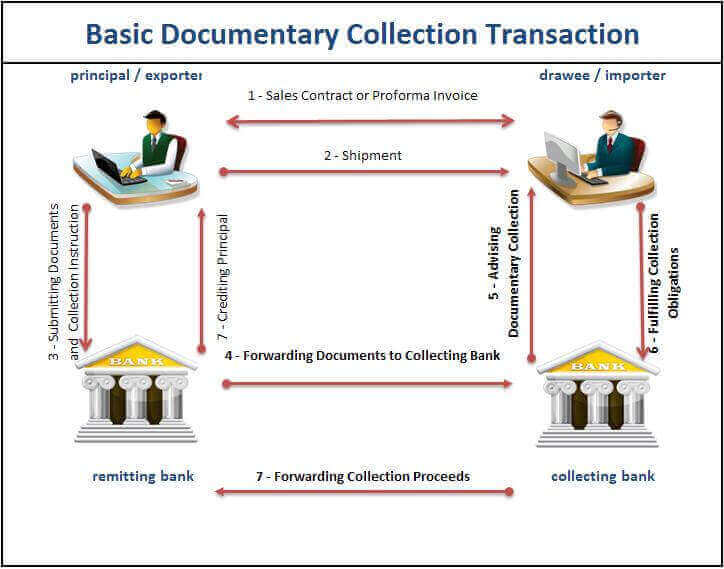

Main parties in a documentary collection and their roles and responsibilities are summarized below:

the “principal” who is the party entrusting the handling of a collection to a bank;

the “remitting bank” which is the bank to which the principal has entrusted the handling of a collection;

the “collecting bank” which is any bank, other than the remitting bank, involved in processing the collection;

the “presenting bank” which is the collecting bank making presentation to the drawee.

the “drawee” is the one to whom presentation is to be made according to the collection instruction.

Documentary Collection Process (Cash Against Document Transaction Flow)

Exporter and importer sign a sales contract indicating the payment method and shipment terms in addition to other details.

The exporter makes the shipment.

The exporter submits the documents and collection instructions to it’s bank with instructions for delivery.

The exporter’s bank sends the documents to the importer’s bank together with the exporter’s instructions.

The importer’s bank reaches out the the importer and informing about the documentary collection.

The importer fulfills his collection obligations and gets the documents from his bank. The importer’s bank hands the documents to the importer on payment or acceptance of a bill of exchange.

The exporter receives payment.

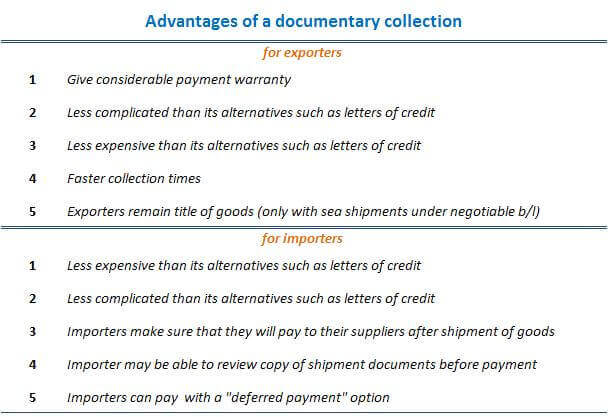

What are the Advantages of a Documentary Collection?

Advantages of a documentary collection can be examined in exporters or importers perspective.

Below figure shows the advantages of a documentary collection for both exporters and importers.

Advantages of a Documentary Collection for Exporters:

Under documentary collections, the documents will not be handed over to the importers unless payment or acceptance of a time draft has been obtained. As importers could not clear goods from the customs without the documents, at least in theory, documentary collections give considerable payment warranty to the exporters.

Documentary collections are less complicated than its alternatives such as letters of credit.

Documentary collections are less expensive than its alternatives such as letters of credit.

Exporters remain the title of goods (only with sea shipments under negotiable b/l) until payment has been received.

Advantages of a Documentary Collection for Importers:

Documentary collections are less expensive than its alternatives such as letters of credit.

Documentary collections are less complicated than its alternatives such as letters of credit.

Under documentary collections, generally, importers make the payment after the shipment of goods.

Importers may be able to review copies of the shipment documents before payment.

Importers may be able to make the payment after they received the documents from their banks by accepting usance bills of exchange (time drafts).

Risks for the Exporters:

Non-Acceptance of Documents Risk: This is one of the major risk factor in a documentary collection for exporters.

Under current documentary collection rules, which are called URC 522, importers are not obligated to collect documents from their banks.

As a result exporters have to understand that upon arrival of the cargo to the importing country, buyers may decide not to pay for the documents and simply left goods unclear at the customs.

Under such a scenario exporters have couple options.

Option 1: Exporters can find another customer to the goods within the country that cargo has arrived. For example if you shipped one container of textile products to Algiers and your buyer do not clear goods from the customs by not having the documents from the bank, then you may try to find another buyer to your goods from Algiers. You may have to give additional discount to make the container attractive to the new buyer.

Option 2: Exporters may try to bring back the container to its home country.

Option 3: Exporters may try to sell the container to the same buyer under more favorable terms.

Non-Payment Risk: Nonpayment risk is the second most frequently seen risk factor in documentary collections.

In most cases we would expect to see a nonpayment risk in a documentary collection which is available by Documents Against Acceptance (D/A).

Nonpayment risk would be happened if the importer accepts a time draft but not be paying on maturity.

“Exporters may seek to have importer’s banks aval to the time draft or bill of exchange in order to eliminate non-payment risk.”

Risk of Delivery of Goods to the Importer without Original Shipment Documents: Importers may clear goods from the customs without having original shipment documents on road, air and rail transportation.

It is also possible for buyers to receive goods from transport companies under sea shipments if express bills of lading (non-negotiable bills of lading) has been utilized.

Under all these conditions as explained above, the importers will be able to receive the goods without the need of original shipment documents, which may lead to a non-payment for the exporters under documentary collections.

Risks for the Importers:

Low Quality Goods Shipment Risk: This is one of the major risk factor in a documentary collection for the importers.

Under current documentary collection rules, which are called URC 522, banks do not check or control the documents.

As a result importers pay for the documents without knowing the quality of the goods.

This risk is higher when the documentary collection is utilized with “documents against payment” (D/P).

Even if the documentary collection is utilized with “documents against acceptance” (D/A), importers may be forced to pay low quality goods according to the local law that governs bill of exchange (draft) procedures.

“Importers can limit their Low Quality Goods Shipment Risk by requesting a pre-shipment inspection from the exporters when working with a new supplier under a documentary collection payment.”

INCOTERMS (International Commercial Terms) have been created by the International Chamber of Commerce in order to reach an uniform set of international rules for the interpretation of trade terms in a global scale.

Pre-Incoterms Era: From Local Practices to Worldwide Trade Rules

Trade, -not only domestic, but also international -, has always been played a key role in development of the civilizations.

Traders follow the local practices, which have been created through hundreds of years.

But these practices have limited sphere of influence, so vital trade customs vary from one place to another.

As international trade emerged it was observed that different practices have been creating ambiguity for the traders.

Frequently, parties to a trade transaction are unaware of the different trading practices in their respective countries.

This can give rise to misunderstandings, disputes and litigation, with all the waste of time and money that this entails.

Buyers and sellers should know exactly what their obligations and rights are in a foreign trade transaction without leaving a possible source of uncertainty.

For example, the place of the delivery, the party who is responsible for making the contract of carriage and insurance, arranging the export and import procedures and paying the loading and unloading costs etc must have been precisely determined.

Additionally, the points indicated above are the core elements of a sales contract, which means that every sales contract must cover these point.

As a result they have to be re-written for every foreign trade transaction.

In order to prevent unnecessary repetitions, trade terms, which contain almost all of the vital parts regarding the obligations of the parties on a sales contract, have been created by various organizations.

But these initial trade terms had different interpretations in different countries, so they could not create an uniformity in practice.

Incoterms Era: Publication of First Incoterms and Revised Versions

INCOTERMS (International Commercial Terms) have been created by the International Chamber of Commerce in order to reach an uniform set of international rules for the interpretation of trade terms in a global scale.

First version of INCOTERMS published in 1936. These first rules were known as “Incoterms 1936”.

International trade terms have been revised regularly by ICC as follows:

Incoterms 1953,

Incoterms 1967,

Incoterms 1976,

Incoterms 1980,

Incoterms 1990,

Incoterms 2000,

Incoterms 2010.

Incoterms 2010 is the latest publication.

Incoterms 2010 published in September 2010 and came into effect on 1 January 2011.

Incoterms 2000

Incoterms 2000 have been released in September 1999 under ICC publication number 560 and have entered into force on 1 January 2000.

Incoterms 2000 defines 13 rules.

Group E

EXW EX WORKS (… named place)

Group F

FCA FREE CARRIER (… named place)

FAS FREE ALONGSIDE SHIP (… named port of shipment)

FOB FREE ON BOARD (… named port of shipment)

Group C

CFR COST AND FREIGHT (… named port of destination)

CIF COST, INSURANCE AND FREIGHT (… named port of destination)

CPT CARRIAGE PAID TO (… named place of destination)

CIP CARRIAGE AND INSURANCE PAID TO (… named place of destination)

Group D

DAF DELIVERED AT FRONTIER (… named place)

DES DELIVERED EX SHIP (… named port of destination)

DEQ DELIVERED EX QUAY (… named port of destination)

DDU DELIVERED DUTY UNPAID (… named place of destination)

DDP DELIVERED DUTY PAID (… named place of destination)

Incoterms 2010

Incoterms 2010 is the latest publication.

Incoterms 2010 published in September 2010 and came into effect on 1 January 2011.

There are 11 rules defined in Incoterms 2010 and they are all trademarked of ICC.

It is possible to purchase both hard copy and online version of Incoterms 2010 rules from ICC’s website.

Explanations of Incoterms 2010 Trade Terms:

The trade terms under Incoterms 2010 have been classified based on modes of transport.

Under Incoterms 2010, 7 trade terms can be used for any mode or modes of transport. These are:

ex works, exw

free carrier, fca

carriage paid to, cpt

carriage and insurance paid to, cip

delivered at terminal, dat

delivered at place, dap

delivered duty paid, ddp

Whereas 4 trade terms under Incoterms 2010 can be used only for sea and inland waterway transport. These are:

free alongside ship, fas

free on board, fob

cost and freight, cfr

cost insurance and freight, cif

On this section I will be explaining the trade terms, which have been defined in Incoterms 2010 rules.

RULES FOR ANY MODE OR MODES OF TRANSPORT

EXW – Ex Works: “Ex Works” means that the exporter delivers the goods to the importer when exporter places the goods at the disposal of the importer at the exporter’s premises or at another named place such as exporter’s warehouse etc.

The exporter does not need to load the goods on any collecting vehicle.

The exporter does not need to clear the goods for export, where such clearance is applicable.

FCA – Free Carrier: “Free Carrier” means that the exporter delivers the goods to the carrier or another person nominated by the importer at the exporter’s premises or another named place.

If the named place is the exporter’s premises, delivery is completed when the goods have been loaded on the means of transport provided by the buyer.

In any other case, delivery is completed when the goods are placed at the disposal of the carrier or another person nominated by the buyer on the seller’s means of transport ready for unloading.

FCA requires the exporter to clear the goods for export, where applicable.

CPT – Carriage Paid to: “Carriage Paid To” means that the exporter delivers the goods to the carrier or another person nominated by the exporter at an agreed place (if any such place is agreed between the parties) and that the seller must contract for and pay the costs of carriage necessary to bring the goods to the named place of destination.

When CPT is used, the exporter fulfills its obligation to deliver when it hands the goods over to the carrier and not when the goods reach the place of destination.

CPT requires the seller to clear the goods for export, where applicable.

CIP – Carriage and Insurance Paid to: “Carriage and Insurance Paid to” means that the seller delivers the goods to the carrier or another person nominated by the seller at an agreed place (if any such place is agreed between the parties) and that the seller must contract for and pay the costs of carriage necessary to bring the goods to the named place of destination.

When CIP is used, the seller fulfills its obligation to deliver when it hands the goods over to the carrier and not when the goods reach the place of destination.

DAT – Delivered at Terminal: “Delivered at Terminal” means that the seller delivers when the goods, once unloaded from the arriving means of transport, are placed at the disposal of the buyer at a named terminal at the named port or place of destination.

“Terminal” includes any place, whether covered or not, such as a quay, warehouse, container yard or road, rail or air cargo terminal.

DAT requires the seller to clear the goods for export, where applicable.

Seller has no obligation to clear the goods for import, pay any import duty or carry out any import customs formalities.

DAP – Delivered at Place: “Delivered at Place” means that the seller delivers when the goods are placed at the disposal of the buyer on the arriving means of transport ready for unloading at the named place of destination.

The seller bears all risks involved in bringing the goods to the named place.

DAP requires the seller to clear the goods for export, where applicable.

Seller has no obligation to clear the goods for import, pay any import duty or carry out any import customs formalities.

DDP – Delivered Duty Paid: “Delivered Duty Paid” means that the seller delivers the goods when the goods are placed at the disposal of the buyer, cleared for import on the arriving means of transport ready for unloading at the named place of destination.

DDP requires the seller to clear the goods for export, where applicable.

Seller has to clear the goods for import, pay any import duty or carry out any import customs formalities.

RULES FOR SEA AND INLAND WATERWAY TRANSPORT

FAS – Free Alongside Ship: “Free Alongside Ship” means that the seller delivers when the goods are placed alongside the vessel (e.g., on a quay or a barge) nominated by the buyer at the named port of shipment.

FAS requires the seller to clear the goods for export, where applicable.

Seller has no obligation to clear the goods for import, pay any import duty or carry out any import customs formalities.

FOB – Free on Board: “Free on Board” means that the seller delivers the goods on board the vessel nominated by the buyer at the named port of shipment or procures the goods already so delivered.

FOB requires the seller to clear the goods for export, where applicable.

Seller has no obligation to clear the goods for import, pay any import duty or carry out any import customs formalities.

CFR – Cost and Freight: “Cost and Freight” means that the seller delivers the goods on board the vessel or procures the goods already so delivered. The risk of loss of or damage to the goods passes when the goods are on board the vessel.

CFR requires the seller to clear the goods for export, where applicable.

Seller has no obligation to clear the goods for import, pay any import duty or carry out any import customs formalities.

CIF – Cost, Insurance and Freight: “Cost, Insurance and Freight” means that the seller delivers the goods on board the vessel or procures the goods already so delivered.

The risk of loss of or damage to the goods passes when the goods are on board the vessel.

The seller must contract for and pay the costs and freight necessary to bring the goods to the named port of destination.

CIF requires the seller to clear the goods for export, where applicable.

Seller has no obligation to clear the goods for import, pay any import duty or carry out any import customs formalities.

What are the Main Differences Between Incoterms 2010 and Incoterms 2000?

There are 4 main differences exist in Incoterms 2010 comparing to Incoterms 2000. These amendments are:

Addition of New Incoterms Rules: Two new incoterms rules have been put into use with the Incoterms 2010 rules. These new rules are DAT and DAP.

Deleted Incoterms Rules: Four incoterms rules have been removed from the usage with the publication of Incoterms 2010. These no longer valid incoterms are DAF, DES, DEQ and DDU.

Changing the Classification of Rules: Incoterms 2010 divides incoterms into two main categories: Rules for any mode or modes of transport (ex works, free carrier, carriage paid to, carriage and insurance paid to, delivered at terminal, delivered at place, delivered duty paid) and rules for sea and inland waterway transport (free alongside ship, free on board, cost and freight, cost insurance and freight)

Definition of New Delivery Place for Incoterms FOB, CFR and CIF: According to Incoterms 2010, the goods will be delivered by exporter to importer only when they will be shipped on board a named vessel at the port of loading. In the previous version of the rules, Incoterms 2000, the goods have been considered as delivered once they have passed the ship’s rail.

How to Use Incoterms 2010 in Letters of Credit?

Incoterms are incorporated into sales contracts or proforma invoices, which are related to the sale of tangible goods.

If an issuing bank adds incoterms into the field 45-A Description of Goods and Services, then the beneficiary must include this exact incoterms phrase in to the commercial invoice.

Otherwise the issuing raises a discrepancy, which is known as incoterms discrepancy.

Example: Usage of Incoterms 2010 in a letter of credit

Field 45A: Description of Goods and Services

HYDROLIC PET BOTTLE BALING AND EQUIPMENT. CONFORM TO PROFORMA INVOICE NUMBER ADG-001 DTD 08.11.2012 CFR ALGIERS PORT-ALGERIA,INCOTERMS 2010 THIS MENTION SHOULD APPEAR ON COMMERCIAL INVOICE.

Commercial Invoice: Includes description of goods including the corresponding incoterms as stated in the letter of credit. (CFR ALGIERS PORT-ALGERIA, INCOTERMS 2010)

Sources:

Incoterms® 2010 English Edition By the International Chamber of Commerce (ICC)

ICC Publication No. 715E, 2010 Edition

The URR 725 are the Uniform Rules for Bank-to-Bank Reimbursements under Documentary Credits ICC publication No. 725.

URR 725 was approved by the ICC national committees at the ICC Banking Commission in April 2008. URR 725 has been effective since 01 October 2008.

URR 725 is an updated version of previous rules for bank-to-bank reimbursements known as URR 525.

The revision was necessary to bring these long-standing rules into conformity with UCP 600, ICC’s universally used rules on letters of credit.

What is the Scope of URR 725?

The Uniform Rules for Bank-to-Bank Reimbursements under Documentary Credits, ICC Publication No. 725, shall apply to any bank-to-bank reimbursement under documentary credits, when the reimbursement authorization expressly indicates that it is subject to these rules.

The rules are binding on all parties thereto, unless expressly modified or excluded by the reimbursement authorization.

How URR 725 Can be Applied to Bank to Bank Reimbursements under Documentary Credits?

The issuing bank is responsible for indicating in the documentary credit that the reimbursement is subject to URR 725.

Under MT700 swift message URR LATEST VERSION or NOTURR are the options regarding reimbursements.

URR LATEST VERSION means that URR rules will apply to the bank to bank reimbursements.

NOTURR means that not URR rules but UCP 600 article 13 will apply to the bank to bank reimbursements..

Table of Contents of URR 725

URR 725 consists of total 17 articles.

URR 725 – Article 1 Application of URR

URR 725 – Article 2 Definitions

URR 725 – Article 3 Reimbursement Authorizations Versus Credits

URR 725 – Article 4 Honour of a Reimbursement Claim

URR 725 – Article 5 Responsibility of the Issuing Bank

URR 725 – Article 6 Issuance and Receipt of a Reimbursement Authorization or Reimbursement Amendment

URR 725 – Article 7 Expiry of a Reimbursement Authorization

URR 725 – Article 8 Amendment or Cancellation of a Reimbursement Authorization

URR 725 – Article 9 Reimbursement Undertaking

URR 725 – Article 10 Standards for a Reimbursement Claim

URR 725 – Article 11 Processing a Reimbursement Claim

URR 725 – Article 12 Duplication of a Reimbursement Authorization

URR 725 – Article 13 Foreign Laws and Usages

URR 725 – Article 14 Disclaimer on the Transmission of Messages

URR 725 – Article 15 Force Majeure

URR 725 – Article 16 Charges

URR 725 – Article 17 Interest Claims/Loss of Value

Definitions from URR 725:

“Reimbursing bank” means the bank instructed or authorized to provide reimbursement pursuant to a reimbursement authorization issued by the issuing bank

“Reimbursement authorization” means an instruction or authorization, independent of the credit, issued by an issuing bank to a reimbursing bank to reimburse a claiming bank or, if so requested by the issuing bank, to accept and pay a time draft drawn on the reimbursing bank.

“Reimbursement undertaking” means a separate irrevocable undertaking of the reimbursing bank, issued upon the authorization or request of the issuing bank, to the claiming bank named in the reimbursement authorization, to honour that bank’s reimbursement claim, provided the terms and conditions of the reimbursement undertaking have been complied with.

“Claiming bank” means a bank that honours or negotiates a credit and presents a reimbursement claim to the reimbursing bank. “Claiming bank” includes a bank authorized to present a reimbursement claim to the reimbursing bank on behalf of the bank that honours or negotiates.

and HAWB (House Air Waybill)?")