Field 20: Documentary Credit Number is a field in MT 700 swift message that is used to indicate the letter of credit number.

This is a mandatory field, which means that it must be stated in all of the letters of credit issued via MT 700 swift format.

This field specifies the documentary credit number which has been assigned by the Sender.

According to ICC Opinions absence of the letter of credit number on the documents is not a valid ground for a refusal.

It should be pointed out that the request for insertion of letter of credit number is usually at the instigation of the issuing bank to facilitate the collation of documents when one or more go astray.

The ICC has commented several times in the past that a refusal based on the absence of a L/C number on a document, where requested in the L/C, is not grounds for a refusal.

MT 700 Field 20: Documentary Credit Number USAGE RULES

This field must not start or end with a slash ‘/’ and must not contain two consecutive slashes ‘//’.

Field 40A: Form of Documentary Credit is a field in MT 700 swift message that is used to indicate the form of the letter of credit.

This is a mandatory field, which means that it must be stated in all of the letters of credit issued via MT 700 swift format.

This field specifies the type of credit.

Codes: One of the following codes must be used

IRREVOCABLE The documentary credit is irrevocable.

IRREVOCABLE TRANSFERABLE The documentary credit is irrevocable and transferable.

MT 700 Field 40A: Form of Documentary Credit USAGE RULES

Details of any special conditions applying to the transferability of the credit and/or the bank authorised to transfer the credit in a freely negotiable credit should be included in field 47A Additional Conditions.

Letter of credit control process for exporters can be grouped under 3 main categories.

Preliminary Investigation Stage: You should check your customer’s background and credibility at this stage.

Sales Contract Stage: You should draft and sign a sales contract at this stage.

Letter of Credit Control Stage: You should control the letter of credit draft at this stage.

Stage 1: Preliminary Investigation Stage:

Learn Who Your Customer Really Is: Nothing can protect you against an ill will customer.

As a result, you need to make sure that your customer is a valid company with a proven track of business and has a financial credibility to complete the transactions.

How to investigate your customer?

In order to understand that you are dealing with a genuine customer, who has a financial strength to start and complete the transaction, you should follow below steps:

Check your customer’s country risk: Customer’s country risk is one of the key elements that you should check before entering any contractual relationship with your customer. Be aware of political risks, economic risks as well as risks associated with sanctions, embargoes and anti money laundering regulations.

Check your customer’s references: Check your customer references by asking the potential customer to the other companies that you have been working with, freight forwarders, custom brokers and governmental organizations such as Commercial Counselors.

Buying a credit report: You can buy credit reports from “International Business Intelligence” companies.

Corporate credit reports tell you how much credibility your customer has.

For example, if the credit report suggests you that you could give 20,000 EUR credit to your customer, while your customer is pushing you to enter into a business with a total amount of 200.000,00 EUR, you should be alerted.

Buying a credit report is a wise thing, working with a new customer, especially when the payment will be made via an open account, documentary collection or letter of credit.

Stage 2: Sales Contract Stage:

After you investigate your customer, you can proceed to the sales contract drafting stage.

Letter of credit is not a sales contract. As a result you must have a sale contract regardless of the payment method you will be choosing.

After checking your customer’s credibility and signing a sale contract, now you can proceed to the letter of credit control phase.

Experienced exporters demand a “draft letter of credit” from the importers in order to make the revisions without paying extra costs for the amendments.

A draft letter of credit is prepared by the issuing bank in swift format contains all the aspects of the actual letter of credit with couple of exceptions.

It is not an operative instrument because the issuing bank intentionally indicates so.

Additionally the draft letter of credit does not secure the issuance of an actual letter of credit.

Step 1 – Checking Irrevocable Structure of the Letter of Credit: Irrevocable means that the issuing bank cannot amend or cancel the letter of credit without the written consent of the beneficiary. Ac per UCP 600 all letters of credit are irrevocable unless otherwise explicitly stated in the credit.

Check and Verify:

Make sure that the letter of credit issued subject to the latest version of the uniform rules of documentary credits, UCP 600.

Make sure that there is no indication in the credit that the letter of credit is “revocable.”

Step 2 – Verifying the Date of Issue, Latest Date of Shipment and Date of Expiry: Each letter of credit should contain a date of issue, latest date of shipment and date of expiry.

Check and Verify:

Make sure that the date of issue indicated in the letter of credit. Some letters of credit states that documents must not be dated before the letter of credit issuance date. You must ensure that if such a clause has been inserted into the credit. If so, you should comply with this regulation.

Make sure that you can make shipment before the latest date of shipment.

Make sure that you can present documents before the expiry date of the letter of credit.

Verify the expiry location of the letter of credit. In order to do that you should check following parts of the MT 700 swift message. “Field 31D: Date and Place of Expiry” and “Field 41a: Available With … By …”

If the letter of credit expires at the counters of the issuing bank, but not in your own country, you may require extra time for forwarding the documents to the issuing bank.

Further Reading:

MT 700 Swift Message Field 41a: Available With … By

MT 700 Swift Message Field 31D: Date and Place of Expiry

MT 700 Swift Message Field 44C: Latest Date of Shipment

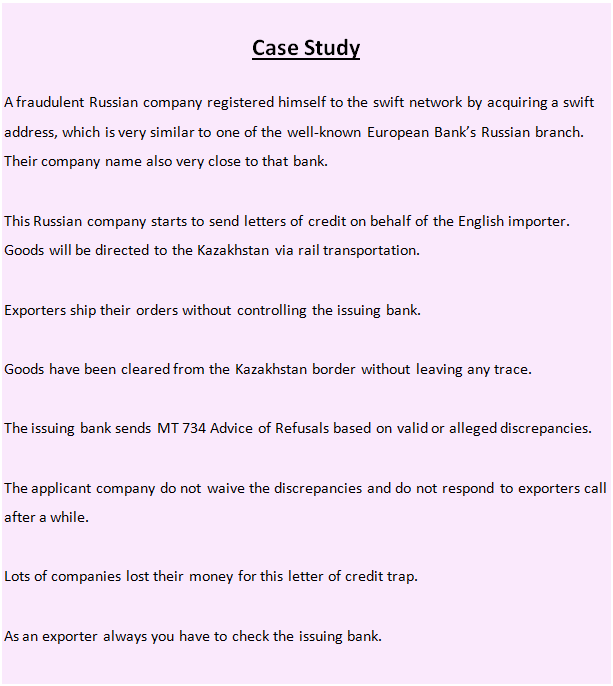

Step 3 – Verifying the Issuing Bank: According to the letter of credit rules non-bank organizations could issue letters of credit, which leaves exporters vulnerable to fraud risk originated from the non-bank letter of credit issuers.

Check and Verify:

Make sure that the issuing bank is a valid and trustworthy bank whom you are comfortable to work with.

Make sure that the advising bank is a reputable bank located in your country.

Make sure that you have received the letter of credit in swift format through an advising bank in your country.

Step 4 – Checking the Beneficiary’s and Applicant’s Name and Address: Issuing banks usually indicate beneficiary’s name and address with errors.

Check and Verify:

Make sure that the full name of your company and its address are correctly stated in the letter of credit.

Make sure that the full name of the importer’s company and its address are correctly stated in the letter of credit.

Further Reading:

MT 700 Swift Message Field 50: Applicant

MT 700 Swift Message Field 59: Beneficiary

Step 5 – Checking the Letter of Credit Currency and Amount: The letter of credit amount and currency must match the amount and currency stated in the sales contract. Be aware of close currency symbols such as USD, AUD, CAD are being shown by the same USD ($) symbol.

Check and Verify:

Make sure that the letter of credit amount is correct.

Make sure that the letter of credit currency is correct.

Further Reading:

MT 700 Swift Message Field 32B: Currency Code, Amount

Step 6 – Checking the Description of Goods/Services: Description of goods and services is very important article especially when completing the commercial invoice.

According to the letter of credit rules, the commercial invoice must contain an exact description of goods and services that the letter of credit states.

Also it is not possible to write additional goods on the invoice even if you mention them free of charge.

Check and Verify:

Make sure that description of goods and services are corresponding the sales contract.

Make sure that all goods have been covered under the commercial invoice.

Further Reading:

MT 700 Swift Message Field 45A: Description of Goods and/or Services

Step 7 – Checking the Documents Requested by the Letter of Credit: Documentation is the core of the letters of credit. Banks decide to pay or reject the presentation by checking the documents only.

If you have a complying set of documents, you will be paid. If your presentation contains discrepancies you will be waiting for the applicant’s approval.

Please give enough attention to the documents which have been covered specifically under the letter of credit rules and international standard banking practices such as transport documents, insurance documents, bills of exchange, commercial invoices, packing lists and certificates.

Check and Verify:

Make sure that you can provide all documents required under the letter of credit.

Make sure that you can comply with the signature, issuance and authentication requirements of the documents.

Make sure that you can supply documents on time.

Make sure that there is no document should be issued or countersigned by the applicant.

Further Reading:

MT 700 Swift Message Field 46A: Documents Required

Letter of Credit Documents

Complying Presentation

How to Handle a Letter of Credit Which Contains a Joker Clause?

What are the Risks of a Document Which is to be Issued, Signed or Countersigned by the Applicant in a Letter of Credit Transaction?

Step 8 – Checking the Payment Terms: Payment terms in a letter of credit transaction define how sooner the beneficiary can reach to the payment. It is also known as “Tenor”.

According to the latest letter of credit rules all letters of credit must state whether they are available by sight payment, deferred payment, acceptance or negotiation.

The payment term “At Sight” indicates that the exporter will be paid within a reasonable time after documents will be found complying by the issuing bank or the confirming bank.

“Deferred Payment” indicates that the exporter will be paid after certain amount of time indicated in the letter of credit.

For example, if a letter of credit indicates that the payment is available at “90 days after bill of lading date”, the exporter will be paid 90 days after date of shipment, of coarse with the condition that the complying presentation.

The payment term “acceptance” indicates that letter of credit consists of a draft either “sight” or “usance”.

The payment term “negotiation” indicates that the beneficiary could get his payment from the nominated bank before the maturity date.

Check and Verify:

Make sure that payment terms quoted in the letter of credit agree with the sales contract.

Further Reading:

Availability of Letters of Credit

At Sight Letter of Credit

Step 9 – Checking the Incoterms: Trade terms have been grouped into two main categories under the Incoterms 2010 rules: Incoterms that can be used only by sea transportation (FAS, FOB, CFR and CIF) and Incoterms that can be used with all modes of transport (EXW, FCA, CPT, CIP, DAT, DAP and DDP).

As a result Incoterms and shipment mode must match each other in a letter of credit transaction.

Furthermore, “Freight Collect” and “Freight Prepaid” expressions must be used in conjunction with the applied Incoterms.

As an example, keep in mind that you can not use the CIF term with “Freight Collect” expression.

Finally, if Incoterms are stated in the “description of goods and services” part of the letter of credit, the commercial invoice must exactly reflect the stated Incoterms.

For example, if the letter of credit states “FOB New York Port, USA, Incoterms 2010” in the “description of goods and services” part of the L/C, the commercial invoice must show this exact definition as indicated.

Check and Verify:

Make sure that Incoterms and the shipment mode must match each other.

Make sure that “Freight Collect” and “Freight Prepaid” expressions are in accordance with the applied Incoterms.

Make sure that you know your responsibilities under the Incoterms which is stated in the letter of credit.

Further Reading:

Incoterms

Incoterms 2000

Incoterms 2010

What happens if a Letter of Credit Calls for a Wrong Incoterms?

Step 10 – Checking the Port of Loading / Port of Discharge: Port of loading and port of discharge are the two main elements of a marine bill of lading.

According to the letter of the credit rules the port of loading and port of discharge must not be in conflict with the ones stated in the letter of credit.

As a result you must make sure that the port of loading and port of discharge is consistent with your sales contract.

Keep in mind that as an exporter you may benefit from the use of a very generalized port of loading definition in the letter of credit , such as “Any U.S. West Coast Port” or “Any U.S. port” or even “Any North American Port”.

But when you dispatch the goods, you must write the actual port of loading to the bill of lading.

Check and Verify:

Make sure that port of loading and port of discharge stated in the letter of credit is consistent with your sales contract.

Further Reading:

MT 700 Swift Message Field 44E: Port of Loading/Airport of Departure

MT 700 Swift Message Field 44F: Port of Discharge/Airport of Destination

Step 11 – Checking the Letter of Credit Fees: Letter of credit is not a cheap payment option.

If you do not give enough attention to the letter of credit charges as an exporter, your profit margin may be reduced significantly.

As a result you have to understand your approximate cost of working with a letter of credit at the beginning of the transaction.

If possible try to reflect these costs into the goods when you are giving a price offer to your customer.

Now you know that letter of credit costs are high, but you may still wonder which letter of credit costs will be paid by the exporter.

In theory all L/C fees must be paid by the importer. But in reality importers pay only letter of credit issuance costs and force exporters to pay the remaining L/C charges.

As a result, exporter may be facing to pay

“Courier Fee / Postage Fee”,

“Advising Fee”,

“Discrepancy Fee”,

“Handling Fee / Negotiation Fee”,

“Amendment Commission”,

“Confirmation Fee”,

“Reimbursing Bank Charges”.

Check and Verify:

Understand and determine which fees must be paid by the exporter according to the letter of credit conditions.

Try to figure out how much money you have to pay for each sort of letter of credit fees.

Further Reading:

Letter of Credit Fees

How to deal with high banking commissions under letters of credit as an exporter

Advising Fee

Discrepancy Fee

Confirmation Fee

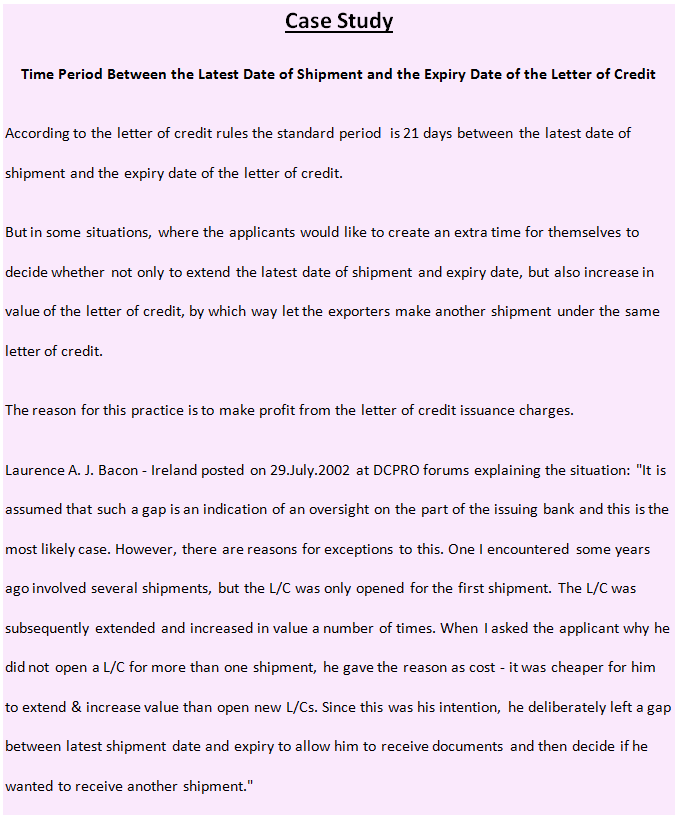

Step 12 – Checking the Presentation Period: Current letter of credit rules gives 21 days to the exporters to make their presentations to the nominated banks.

The 21 days presentation period starts with the date of shipment. You must complete your presentation within this allowed time frame.

In some instances issuing banks arrange special presentation periods for each letter of credit by inserting clauses such as “Documents must be presented for negotiation within 15 days after the on board validation date of the ocean bill of lading and within the validity of the letter of credit.”

If a letter of credit contains a special presentation period clause, the exporter must obey this specific presentation period for the letter of credit, but not the standard 21 day presentation period.

Check and Verify:

Determine the presentation period of the letter of credit.

Make sure that you are able to comply with this presentation stipulation.

Further Reading:

MT 700 Swift Message Field 48: Period for Presentation

Step 13 – Checking the Partial Shipments: The letter of credit rules allow partial shipments.

Able to make partial shipments is a huge advantage for the exporter. As a result you should try to keep the letter of credit in a way that it is allowing the partial shipments.

If your letter of credit is silent concerning partial shipments, it is should be understood that the partial shipments are allowed.

Check and Verify:

Make sure that partial shipments are allowed under the letter of credit and it is what you have agreed on your sales contract.

Further Reading:

What is a partial shipment?

MT 700 Swift Message Field 43P: Partial Shipments

Which one is more important: Partial shipment or transshipment?

Do partial drawings and partial shipments have the same meaning?

What are the consequences of not allowing partial shipments?

Step 14 – Checking the Transshipment: The letter of credit rules allow transshipments.

Actually, transhipments are not controlled by the exporters and almost all the container carriers do practice several transshipments between the ports of loading and ports of discharge.

For example a container vessel carrying cargo between Xiamen Port, China to Ploce Port, Croatia make transshipments at Chiwan Port, China and Gioia Tauro Port, Italy.

These transshipments are arranged by the carrier. The shipper has no influence.

You cannot say to the carrier “Hey, transhipment is prohibited as per my letter of credit terms, you can not make any transshipments!”.

What you can do is to make sure that transshipment is allowed under your letter of credit.

Transhipment should be prohibited only very rare situations in the letter of credit transactions.

Check and Verify:

Make sure that transshipments are allowed under the letter of credit and it is what you have agreed on your sales contract.

Step 15 – Checking the Reimbursement Instructions: Reimbursement instructions can be found either in;

“Field 47-A : Additional Conditions” or

“Field 78: Instructions to the Paying/Accepting/Negotiating Bank”.

Reimbursement instructions are very important to the exporter, as they determine how and when payment will be received.

There are mainly four types of reimbursement instructions used in international documentary credits. These are:

The issuing bank authorizes the nominated bank to debit its account;

The issuing bank instructs the nominated bank to claim reimbursement from a reimbursing bank;

The issuing bank requires the nominated bank to send a swift message notifying the issuing bank that the documents have been received and found to be in compliance with the LC terms, only then the issuing bank remits funds to the nominated bank;

The issuing bank requires nominated bank to send documents to the issuing bank for payment (very rare and slowest reimbursement method of payment).

Check and Verify:

Make sure that reimbursement instructions do not block you to receive payment via unreasonable restrictions.

Further Reading:

MT 700 Swift Message Field 78: Instructions to the Paying/Accepting/Negotiating Bank

URR 725 – The Uniform Rules for Bank-to-Bank Reimbursements under Documentary Credits – ICC Publication No. 725

Step 16 – Non-Documentary Conditions: A non-documentary condition can be defined as any instruction or condition that is not clearly attributable to a document to be stipulated in a documentary credit.

Non-documentary conditions are great source of confusion and disputes between the issuing banks and exporters.

Documentary Condition Examples:

Certificate of origin issued in 1 original and 1 copy legalized by the local chamber of commerce attesting that goods are of China origin.

Certificate of origin must show that goods are of China origin.

Non-Documentary Condition Examples:

Exported goods must be Australian Origin.

Any of the presented document must not show that goods are originated from a country other than Australia.

Check and Verify:

Make sure that you have identified all non-documentary conditions in the letter of credit.

What are the Risks of a Document Which is to be Issued, Signed or Countersigned by the Applicant in a Letter of Credit Transaction?

Step 18 – Checking the Confirmation: Confirmation means a definite undertaking of the confirming bank, in addition to that of the issuing bank, to honour or negotiate a complying presentation.

A confirming bank is requested by the issuing bank to add its guarantee of payment or acceptance to the letter of credit instrument.

You can protect yourselves against various risks under the letter of credit transaction by having the letter of credit confirmed by a prime bank in your country.

Check and Verify:

Make sure that you can have the letter of credit confirmed by one of the prime banks in your country.

Step 19 – Checking the Reimbursement Bank: The reimbursing bank is usually named in “Field 53a: Reimbursing Bank” of a S.W.I.F.T. 700 message.

Check and Verify:

Make sure that reimbursement bank identified in the letter of credit is one of the most reputable banks around the world such as Commerzbank, HSBC Bank, The Bank of America Merrill Lynch etc..

Further Reading:

MT 700 Swift Message Field 53a: Reimbursing Bank

MT 700 Swift Message Field 78: Instructions to the Paying/Accepting/Negotiating Bank

Reimbursement and Reimbursing Bank

URR 725 – The Uniform Rules for Bank-to-Bank Reimbursements under Documentary Credits – ICC Publication No. 725

Step 20 – Conclusion: Do not assume anything when working with a letter of credit.

Always act with caution. If you do not know a term read the letter of credit rules, ask it to your bank, check reputable online sources before taking any further steps.

Let me finish this part with the sentence I have written just at the beginning of this booklet.

“Both exporters and importers are protected by letters of credit in certain amount, if they act properly.”

Shipping documents, when used as a term in a letter of credit, could create problems between the issuing bank and the beneficiary due to its obscure meaning.

It is not possible to find a “shipping documents” term under the documentary credit rules, as a result ICC Banking Commission discourages banks to use it.

But issuing banks still choose to implement this term in their credits one way or another..

You can find two examples below how shipping documents term is used in the letters of credit by the issuing banks.

Example 1:

Field 47-A Additional Conditions: Shipment date and shipping documents including bill of lading dated prior to letter of credit opening date is not acceptable.

Analysis: Using the shipping documents term in a way, as specified on above example, may create disputes between the issuing bank and the beneficiary.

According to the ISBP 745, which is the latest International Standard Banking Practices published by ICC, “shipping documents” term defined as follows: “all documents required by the credit, except drafts, tele‐transmission reports and courier receipts, postal receipts or certificates of posting evidencing the sending of documents.”

Conclusion: Under normal circumstances, it is expected that even if the drafts, tele‐transmission reports and courier receipts, postal receipts or certificates of posting have been dated prior to the issuance date of the credit, the issuing bank would accept such presentation.

These having been said, in order to be on the safe side, the beneficiary may choose to present all documents under this letter of credit will be dated after the issuance date of the documentary credit to prevent any problem with the issuing bank, because of the fact that the issuing bank’s intention, by using the term of shipping documents, may be referring all the documents that have been requested by the credit, but not just the ones as being described under the ISBP 745.

Example 2:

46-A Documents Required:

Full set of clean on board bills of lading issued or endorsed to the order of Issuing Bank, notify applicant showing freight prepaid.

Field 47-A Additional Conditions: Shipping documents should be prepared in the name of: Applicant Company.

Analysis: Using the “shipping documents” term in a way as exhibited in example 2 would be the most risky situation for the beneficiaries.

Let me try to explain the reason.

On this example, the issuing bank defines how the bills of lading should be completed under the field 46-A: Documents Required.

But the issuing bank puts another indication under the field 47-A Additional Conditions stating that “Shipping documents should be prepared in the name of: Applicant Company.”

The beneficiary may confuse at the document preparation stage as these statements contradict each other.

Under such a circumstances the best advice that can be given to the beneficiary is that applying to the applicant for an amendment to delete the so called phrase which has been inserted in field 47-A by the issuing bank.

Date of shipment is one of the key definitions in a letter of credit transaction. It is used to determine

whether shipment made on time or not (in other words a late shipment has been effected or not)

whether documents presented within the presentation period or not (in other words a late presentation has been effected or not)

maturity date of the time draft

maturity date of a deferred payment letter of credit.

Date of shipment on a bill of lading can be determined in two ways.

In the first scenario, we will face a situation where a bill of lading does not contain any dated shipped on board notation.

In the second scenario, we will be having a bill of lading which contains a dated shipped on board notation.

Option 1 =>There is no shipped on board notation exists on the bill of lading:

The date of issuance of the bill of lading will be deemed to be the date of shipment.

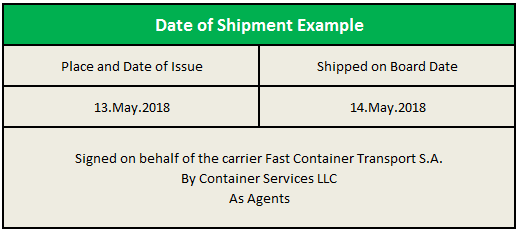

Option 2=>Bill of lading indicates, by stamp or notation, a shipped on board date:

Notation date will be deemed to be the date of shipment as specified below: Date of shipped on board notation/stamp => this date will be deemed to be the date of shipment

Example: On the below figure, you can see a shipped on board notation which is located on the bottom of a bill of lading. As there is a dated on board notation exist on the bill of lading, date of shipment will be deemed to be this shipped on board notation date which is 14.May.2018.

whether shipment made on time or not (in other words a late shipment has been effected or not),

whether documents presented within the presentation period or not (in other words a late presentation has been effected or not),

maturity date of the time draft,

maturity date of a deferred payment letter of credit.

Using Date of Shipment in Order to Determine Whether Shipment Has Been Made on Time or Not:

If a letter of credit calls for an original transport document, it is also expected that the letter of credit indicates a latest date of shipment.

In this regard, it is of paramount importance to clarify which documents are considered as a transport document under the letter of credit rules:

Transport Documents Under the Letter Of Credit Rules: Below you can find the transport documents defined under the letter of credit rules.

Transport Document Covering at Least Two Different Modes of Transport (multimodal bill of lading or combined transport document etc…)

Bill of Lading (marine bill of lading, ocean bill of lading etc..)

Non-Negotiable Sea Waybill

Charter Party Bill of Lading

Air Transport Document (Air Waybill)

Road, Rail or Inland Waterway Transport Documents

Courier Receipt, Post Receipt or Certificate of Posting

If one of the transport documents is requested in the credit, the beneficiary must complete the shipment before the latest date of shipment. Otherwise the issuing bank finds the presentation not complying and raises a late shipment discrepancy.

Using Date of Shipment in Order to Determine Whether Documents Have Been Presented Within the Presentation Period or Not:

A presentation including at least one original transport document, which can be a multimodal bill of lading, combined transport document, bill of lading, non-negotiable sea waybill, charter party bill of lading, air transport document, road transport document, rail transport document, inland waterway transport document, courier receipt, post receipt or certificate of posting, must be made not later than 21 calendar days after the date of shipment.

In any case presentation must be made not later than the expiry date of the credit.

Using Date of Shipment to Determine Maturity Date of the Time Draft:

Letter of credit that has been issued available by acceptance of a time draft may specify a maturity date which will be calculated with the help of the date of shipment.

Let me give you a couple of examples:

at 60 days after the bill of lading date

at 90 days after bill of lading

after 30 days from date of bill of lading

When the tenor of the bill of exchange refers to, for example, 30 days after the bill of lading date, the on board date is deemed to be the bill of lading date.

On this occasion the on board date could be prior to or later than the issuance date of the bill of lading.

Using Date of Shipment to Determine Maturity Date of a Deferred Payment Letter of Credit:

Letter of credit that has been issued available by deferred payment may specify a maturity date which will be calculated with the help of the date of shipment.

Let me give you couple of examples as follows:

deferred payment at 60 days after the bill of lading date

deferred payment at 90 days after bill of lading

deferred payment after 30 days from date of bill of lading

When tenor or maturity date of the deferred payment refers to, for example, 30 days after the bill of lading date, the on board date is deemed to be the bill of lading date.

On this occasion the on board date could be prior to or later than the issuance date of the bill of lading.

Transferable letters of credit are a tool used by trading companies, or other third parties, to facilitate a trade transaction. (1)

Transferable letters of credit are sort of documentary credits which can be used in situations where middlemen are playing a certain role.

How Does a Transferable Letter of Credit Work:

Usually middlemen (first beneficiaries) do not have enough capital establishment to buy the goods from their sources (second beneficiaries) before they re-sell them to their final customers (applicants).

If the final buyer finds it valuable working with a middleman, then he can let the middleman benefit from his credibility by supplying him a transferable letter of credit.

The middleman have the part or all of the transferable letter of credit transferred to his supplier, who has gained considerable payment assurance to ship the goods.

The supplier can receive its payment portion in exchange for the complying documents stated in the letter of credit.

The middleman is entitled to substitute its own invoice for the one that is presented by the supplier and collects the difference as his profit.

Transferable Credits:

Transferable letter of credit is a special type of l/c which is suitable for triangle trade.

Triangle trade is a type of international business transaction in which a middleman sits between exporter and importer.

Middlemen or trade brokers have limited finance facilities. As a result, they have to rely on their buyers’ finance support such as a transferable letter of credit.

Process of the transferable lc is as follows in a very simple term. Middleman’s buyer open a transferable letter of credit in favor of the middleman. Then middleman transfers a part of this l/c to his supplier. The difference between two l/cs is the net profit margin of the middleman.

Banks play a key role on transferable letters of credit.

UCP 600 rules have special articles about transferable letters of credit.

Letter of Credit Rules Regarding Transferable Credits:

According to the latest letter of credit rules, UCP 600 Article 38 which is titled as Transferable Credits

a. A bank is under no obligation to transfer a credit except to the extent and in the manner expressly consented to by that bank.

b. For the purpose of above mentioned article you can find some important definitions of transferable letters of credit as follows:

Transferable credit means a credit that specifically states it is “transferable”. A transferable credit may be made available in whole or in part to another beneficiary (“second beneficiary”) at the request of the beneficiary (“first beneficiary”).

Transferring bank means a nominated bank that transfers the credit or, in a credit available with any bank, a bank that is specifically authorized by the issuing bank to transfer and that transfers the credit. An issuing bank may be a transferring bank.

Transferred credit means a credit that has been made available by the transferring bank to a second beneficiary.

c. Unless otherwise agreed at the time of transfer, all charges (such as commissions, fees, costs or expenses) incurred in respect of a transfer must be paid by the first beneficiary.

d. A credit may be transferred in part to more than one second beneficiary provided partial drawings or shipments are allowed.

A transferred credit cannot be transferred at the request of a second beneficiary to any subsequent beneficiary. The first beneficiary is not considered to be a subsequent beneficiary.

e. Any request for transfer must indicate if and under what conditions amendments may be advised to the second beneficiary. The transferred credit must clearly indicate those conditions.

f. If a credit is transferred to more than one second beneficiary, rejection of an amendment by one or more second beneficiary does not invalidate the acceptance by any other second beneficiary, with respect to which the transferred credit will be amended accordingly. For any second beneficiary that rejected the amendment, the transferred credit will remain unamended.

g. The transferred credit must accurately reflect the terms and conditions of the credit, including confirmation, if any, with the exception of:

– the amount of the credit,

– any unit price stated therein,

– the expiry date,

– the period for presentation, or

– the latest shipment date or given period for shipment,

any or all of which may be reduced or curtailed.

The percentage for which insurance cover must be effected may be increased to provide the amount of cover stipulated in the credit or these articles.

The name of the first beneficiary may be substituted for that of the applicant in the credit.

If the name of the applicant is specifically required by the credit to appear in any document other than the invoice, such requirement must be reflected in the transferred credit.

h. The first beneficiary has the right to substitute its own invoice and draft, if any, for those of a second beneficiary for an amount not in excess of that stipulated in the credit, and upon such substitution the first beneficiary can draw under the credit for the difference, if any, between its invoice and the invoice of a second beneficiary.

i. If the first beneficiary is to present its own invoice and draft, if any, but fails to do so on first demand, or if the invoices presented by the first beneficiary create discrepancies that did not exist in the presentation made by the second beneficiary and the first beneficiary fails to correct them on first demand, the transferring bank has the right to present the documents as received from the second beneficiary to the issuing bank, without further responsibility to the first beneficiary.

j. The first beneficiary may, in its request for transfer, indicate that honour or negotiation is to be effected to a second beneficiary at the place to which the credit has been transferred, up to and including the expiry date of the credit. This is without prejudice to the right of the first beneficiary in accordance with sub-article 38 (h).

k. Presentation of documents by or on behalf of a second beneficiary must be made to the transferring bank.

References:

A guide to doing business abroad, International Trade Procedures, Wells Fargo, P:28

On this post, you can find explanations regarding the latest date of shipment and expiry date.

If a letter of credit requests presentation of a transport document and a latest date of shipment indicated in the credit; then the shipment must be completed on or before the latest date of shipment indicated in the credit.

If a letter of credit requests presentation of a transport document but not indicated a latest date of shipment; then the shipment and the presentation must be completed on or before the expiry date indicated in the credit.

According to the letter of credit rules, a presentation including one or more original transport documents subject to articles 19, 20, 21, 22, 23, 24 or 25 must be made by or on behalf of the beneficiary not later than 21 calendar days after the date of shipment as described in these rules, but in any event not later than the expiry date of the credit.

Latest Date of Shipment:

Latest date of shipment is an optional information and not every letter of credit issued in swift format contains a latest date of shipment.

Latest date of shipment can be meaningful only if the letter of credit requests presentation of a transport document. No transport document, no meaning of the latest date of shipment.

If the letter of credit indicates a latest date of shipment, then the beneficiary has to complete the shipment of goods on or before this date.

The beneficiary has to present a transport document showing a shipment date on or before the latest date of shipment in order to prove his compliance with the latest date of shipment.

If the beneficiary presents a transport document showing a shipment date later than the latest date of shipment, then the issuing bank raises a “late shipment discrepancy“.

Expiry Date :

The beneficiary has to present the documents to nominated bank on or before the expiry date of the l/c.

If the beneficiary can not make the presentation on time, the letter of credit will be terminated and will not be valid any more.

Irrevocable letter of credit (ILOC) is a type of documentary credit which can not be cancelled or amended by the issuing bank without the agreement of the parties of the letter of credit transaction.

The letter of credit world is full of misunderstandings, improper industry practices including irregular banking practices, false information and so on.

Irrevocable letter of credit term is not an exception.

Many traders attribute irrelevant or false meanings to this term.

Let me give you a quick example: A trade manager once told me that he will secure the payment from his bank as long as he will receive an irrevocable letter of credit from his buyer.

He was mistakenly believing that the irrevocable letter of credit give him %100 payment assurance. But this is not true.

Definition of an Irrevocable Letter of Credit?

We can define an irrevocable letter of credit (ILOC) as a type of documentary credit which can not be cancelled or amended by the issuing bank without the agreement of the parties of the letter of credit transaction.

Table 1 shows the parties to the irrevocable letter of credit transaction.

If the letter of credit is confirmed, then the parties of the letter of credit are the issuing bank, confirming bank and the beneficiary.

If the letter of credit is not confirmed, then only the issuing bank and the beneficiary are the parties of the irrevocable letter of credit transaction.

Table 1 : Parties to the irrevocable letter of credit

Issuing bank can not cancel or amend an unconfirmed irrevocable letter of credit without the written consent of the beneficiary.

Issuing bank can not cancel or amend a confirmed irrevocable letter of credit without the written consent of the beneficiary and the confirming bank.

As illustrated above, the beneficiary of an irrevocable letter of credit knows that the terms and conditions of the credit can not be changed without his approval.

Also, he knows that the l/c will not be cancelled either.

But does this mean that the beneficiary have %100 payment guaranty under an irrevocable l/c. As I said earlier. No.

Let me write down my reasons,

Letter of credit is a conditional payment method. In order to be getting paid under a letter of credit, irrevocable or revocable, the beneficiary has to make a complying presentation. In simple words, the beneficiary has to make the shipment and collect all trade documents requested under the l/c and present them to the issuing bank (nominated bank or confirming bank in some cases). Afterwards, the issuing bank will check the documents and pays the credit amount to the beneficiary only if the documents are found to be compliant.

If issuing bank finds that the documents are non-compliant, then the issuing bank will send an advice of refusal to the beneficiary. The issuing bank sends the advice of a refusal as a swift message, MT 734 Advice of a Refusal.

Once the beneficiary has received the advice of the refusal from the issuing bank, he has 3 options.

If the beneficiary has still enough time to correct the documents, he may try to do so by submitting new documents. But it is mostly not possible due to two major time constraints for a new presentation: The expiry date of the letter of credit and period for presentation of the documents.

The second option of the beneficiary would be to apply the importer to accept the discrepancies.

The final option would be recalling the documents from the issuing bank and trying to find a new buyer to the goods.

Conclusion:

A revocable letter of credit may be amended or cancelled by the issuing bank at any moment and without prior notice to the beneficiary.

Irrevocable letter of credit, on the other hand, can not be cancelled or amended by the issuing bank without the agreement of the parties of the letter of credit transaction.

According to the latest letter of credit rules (UCP 600) all credits are irrevocable.

Letter of credit is a conditional payment obligation of the issuing bank and the beneficiary always has to make a complying presentation in order to receive the payment.

Bill of exchange, which is also known as draft, is a financial document commonly used in international trade transactions.

According to UK’s Bill of Exchange Act (1882), the bill of exchange defined as an “unconditional order in writing, addressed by one person to another, signed by the person giving it (drawer), requiring the person to whom it is addressed (drawee) to pay on demand or at a fixed or determinable future time a sum certain in money to or to the order of a specified person (payee), or to bearer”.

Parties to a Bill of Exchange:

Drawer of a Bill of Exchange / Draft: Is the party that issues a Bill of Exchange in an international trade transaction; usually the seller or exporter.

Drawee of a Bill of Exchange / Draft: Is the recipient of the Bill of Exchange for payment or acceptance in an international trade transaction; usually the importer or importer’s bank.

Payee of a Bill of Exchange / Draft: Is the party to whom the Bill is payable; usually the seller or his bank.

How Does a Bill of Exchange Work in the Documentary Collections?

Documentary Collection (D/C) is a payment method in international trade. Documentary collection is also known as Cash Against Documents (CAD).

There are two payment options available in the documentary collections: Documents Against Payment (D/P) and Documents Against Acceptance (D/A).

Under the documents against payment option, it is not advisable to use a bill of exchange. The importer should make the payment at sight against the documents.

Under the documents against acceptance (D/A) payment option, it is advisable to use a bill of exchange payable at a future date (time draft).

Bill of Exchange Workflow in the Documentary Collections:

The bill of exchange workflow under documents against acceptance (D/A) payment option is as follows:

The exporter issues a bill of exchange payable at a future date (time draft) along with other shipping documents and sends it to the importer via his bank on collection basis.

The importer applies to his bank, accepts the bill of exchange, receives the documents, clears the goods from the customs and makes the payment at the maturity date of the bill of exchange.

How Does a Bill of Exchange Work in the Letters of Credit?

There are four payment options available in the letters of credit: Sight payment, acceptance, deferred payment and negotiation.

It is not possible to use a bill of exchange in the letters of credit, which are available by deferred payment.

On the other hand, every letter of credit that is issued available by acceptance must demand presentation of a bill of exchange along with other shipping documents.

Under sight payments and negotiation, the bill of exchange may or may not be used.

Bill of Exchange Workflow in the Letters of Credit:

The bill of exchange workflow in the letters of credit available by sight payment, acceptance or negotiation is as follows:

Sight Payment:

After making the shipment, the exporter collects all the shipping documents and issues an at sight bill of exchange to make the presentation to the issuing bank or confirming bank or nominated bank, as applicable.

If the bank determines that the presentation is complying, then pays the credit amount to the beneficiary.

Acceptance:

After making the shipment, the exporter collects all the shipping documents and issues a time draft (bill of exchange payable at a future date) to make the presentation to the issuing bank or confirming bank or nominated bank, as applicable.

If the bank determines that the presentation is complying, then accepts the time draft and pays the credit amount to the beneficiary at maturity.

Negotiation:

The letters of credit available by negotiation can be payable at sight or usance.

If the letter of credit requires an at sight bill of exchange, the process will be the same as the sight payment.

If the letter of credit requires presentation of a time draft, the process will be the same as the acceptance.

Conclusion:

Bill of exchange plays an important role in commercial and financial cycles not only as a method of payment or a way of providing credit, but also as security for payments. (1)

Bill of exchange mainly used in documentary collections and letters of credit.

Under the documentary collections, the bill of exchange can be used only when Documents Against Acceptance (D/A) payment option is chosen.

Under the documentary collections, the bill of exchange payable at a future date (time draft) drawn on the importer. The importer accepts the bill of exchange, receives the documents, clears the goods from the customs and makes the payment at the maturity date of the bill of exchange.

If the importer does not pay the bill of exchange amount at maturity, the exporter tries to use his legal rights that is stem from the bill of exchange.

Under the documentary collections, the importer’s banks has no payment obligation unless the bill of exchange has been avalized by the importer’s bank.

Under the letters of credit, the bill of exchange can be used with at sight, acceptance and negotiation payment options.

Under the letters of credit, the bill of exchange can be issued at sight or payable at a future date (time draft).

Under the letters of credit, the bill of exchange must be drawn on a bank that is specified in the credit.

Under the letters of credit, the bill of exchange does not give additional payment guarantee to the beneficiary, whereas the situation will be different for the banks. Bill of exchange may change the payment obligation between the nominated bank and the issuing bank; the confirming bank and the issuing bank etc.

References:

Bills of Exchange, A Guide to Legislation in European Countries, Dr. jur. Uwe Jahn, ICC Publication No 531 (E), 1996, P:3