Bill of lading is a very important transport document, because it is suppose to evidence of contract of carriage, a receipt of goods by the carrier and a document of title to the goods.

In order a bill of lading functions as it is suppose to function, it must be completed and signed by a reliable carrier.

According to the current letter of credit rules a bill of lading must identify the name of the carrier and be signed by carrier, master or their agents.

A bill of lading, however named, must appear to indicate the name of the carrier and be signed by:

the carrier or a named agent for or on behalf of the carrier, or

the master or a named agent for or on behalf of the master.

If the issuing bank finds out that the name of the carrier not identified on the bill of lading, then the issuing bank will raise a “Carrier Not Identified” discrepancy.

If the issuing bank finds out that the bill of lading has not been signed by the carrier, master or their named agents on behalf of either the carrier or master, then the issuing bank will raise a “Bill of Lading not Signed as per UCP” discrepancy.

Example of Carrier Not Identified Discrepancy:

A letter of credit has been issued in SWIFT format, subject to UCP latest version, with the following details:

Letter of Credit Conditions

Field 46A: Documents Required: Full set of shipped on board bill of lading marked freight collect made out to order of Commercial Bank of Kuwait notify Applicant Company with full address and contact details as indicated in the credit.

Bill of Lading

The beneficiary presented a bill of lading in which carrier name not identified. Issuing bank raises carrier not identified discrepancy.

2.Example of Bill of Lading not Signed as per UCP Discrepancy:

A letter of credit has been issued in SWIFT format, subject to UCP latest version, with the following details:

Letter of Credit Conditions

Field 46A: Documents Required: Full set of shipped on board bill of lading marked freight prepaid made out to order of Burgan Bank, Kuwait notify Applicant Company with full address and contact details as indicated in the credit.

Bill of Lading

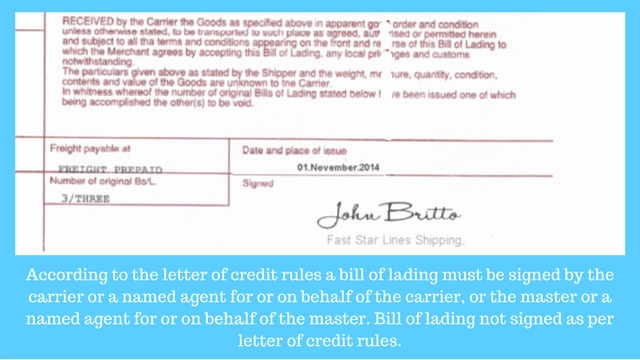

The beneficiary presented a bill of lading, which is signed as seen on the below picture.

According to letter of credit rules a bill of lading must be signed by the carrier or a named agent for or on behalf of the carrier, or the master or a named agent for or on behalf of the master. Sample bill of lading not signed as per letter of credit rules, UCP 600.

The issuing bank raises bill of lading not signed as per UCP discrepancy.

A clean bill of lading is a type of transport document, which bears no clause or notation, which expressly declares a defective condition of the goods and/or the packaging.

Banks can accept only clean transport documents under letters of credit transactions.

Banks do not accept any unclean transport document.

As a result, presentation of an unclean bill of lading would create a discrepancy, in the eyes of the banks.

What makes a bill of lading clean or unclean?

An express clause declares a defective condition of the goods makes the bill of lading unclean.

An express clause declares a defective condition of the packages of the goods makes the bill of lading unclean.

Please kindly keep in mind that below points do not make a bill of lading unclean.

Absence of the word “clean” does not make a bill of lading unclean.

Deletion of the word “clean” does not make a bill of lading unclean.

Sample Clauses Which Make a Transport Document Unclean:

Packaging is not sufficient for port to port ocean transportation.

Goods which improperly stored at the port of loading have been shipped on board partially wet and not in good condition.

Example of an Unclean Bill of Lading Discrepancy:

A letter of credit has been issued in SWIFT format, subject to UCP latest version, with the following details:

Letter of Credit Conditions

Field 45A: Description of Goods and or Services: Fruits

Field 46A: Documents Required: Full set of clean on board bill of lading marked freight payable at destination made out to order of Bankinter, SA notify Applicant Company with full address and contact details as indicated in the credit.

Bill of Lading

The beneficiary presented a bill of lading with the following clause: Packaging is not sufficient for the sea journey.

Discrepancy: Unclean bill of lading presented.

Reason for Discrepancy: A bank will only accept a clean transport document. A clean transport document is one bearing no clause or notation expressly declaring a defective condition of the goods or their packaging.

How to Prevent an Unclean Bill of Lading Discrepancy:

Do not focus on “Clean” word, that might be stated on the credit. A clean bill of lading need not to indicate “clean on board” notation. “Shipped on board” notation is enough.

Make sure that, the shipment is effected in a sound way. The goods are packed well, secured inside the container and there is no leakage out of the container.

If you are going to make a bulk shipment, make sure that the goods will not be affected from bad weather.

Speak with your logistics provider, in advance of the shipment, and learn all necessary precautions that you need to take, in order to prevent an unclean bill of lading issuance.

The importer and exporter should determine, when signing the sales contract, to allow or prohibit partial shipments.

Partial shipment can be defined as shipping the goods not whole at once, but in more than one smaller shipments.

Partial shipments total may be less than the total contract amount.

The letter of credit rules allow partial shipments and partial drawings. But, in some occasions, issuing banks tend to restrict partial shipments.

In order to understand, whether or not partial shipments are allowed under a documentary credit, you need to look at “Field 43P: Partial Shipments” within the swift message body.

Field 43P: Partial Shipments: Allowed means that partial shipments are permitted

Field 43P: Partial Shipments: Not Allowed means that partial shipments are not permitted.

If the issuing bank finds out that partial shipments have been effected, although the letter of credit prohibits partial shipments, then the issuing bank will raise a discrepancy, which is known as partial shipments discrepancy.

Sample Partial Shipment Discrepancy on a Bill of Lading under a Letter of Credit:

A letter of credit has been issued in SWIFT format, subject to UCP 600, with the following details:

Letter of Credit Conditions

Field 43P: Partial Shipments: Not Allowed

Field 43T: Transhipment: Not Allowed

Field 45-A: Description of Goods: 24 Pcs of Food Sorting Machinery

Field 46A: Documents Required: Full set of original bill of lading laden on board marked freight collect made out to the order of HSBC Bank, USA notify applicant.

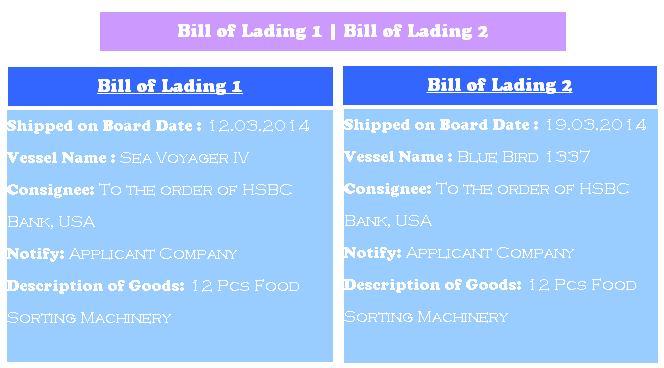

The beneficiary presented two set of documents containing two bills of lading among other documents with the following data:

Discrepancy: Partial Shipment Effected.

Reason for Discrepancy: The beneficiary presented two sets of documents within the same presentation. The issuing bank determined that partial shipment has been effected on contrary to the letter of credit terms, because goods have been dispatched with two different vessels.

How to Prevent a Partial Shipment Discrepancy?

Check the letter of credit before shipment of goods, in order to determine whether or not partial shipment is prohibited.

If partial shipment is allowed, you can make smaller shipments until you reach total letter of credit amount. Be careful with the latest date of shipment.

If partial shipment is not allowed, but your intention to do so; then you must get in touch with your customer to amend the letter.

In a letter of credit transaction, the gross weight must show the same value on all presented documents.

As an example, the gross weight on the bill of lading must not conflict with the gross weight stated on the packing list, weight list or any other document.

According to the letter of credit rules, a data in a document, when read in context with the credit, the document itself and international standard banking practice, need not be identical to, but must not conflict with, data in that document, any other stipulated document or the credit.

If the issuing bank finds out that the gross weight on bill of lading and packing list do not match, then the issuing bank will raise a discrepancy, which is known as the gross weight is different on the bill of lading than the gross weight stated on the packing list.

Discrepancy Example: Gross Weight is Different on the Bill of Lading Than the Gross Weight Stated on the Packing List under a Letter of Credit:

A letter of credit has been issued in SWIFT format, subject to UCP latest version, with the following details:

Letter of Credit Conditions

Field 43P: Partial Shipments: Allowed

Field 43T: Transhipment: Allowed

Field 45-A: Description of Goods: 24,000,00 KGS Textile Dyeing Chemicals

Field 46A: Documents Required:

Full set of original bill of lading laden on board marked freight collect made out to the order of Citibank, USA notify applicant.

Packing list one original and one copy.

Commercial invoice in three originals.

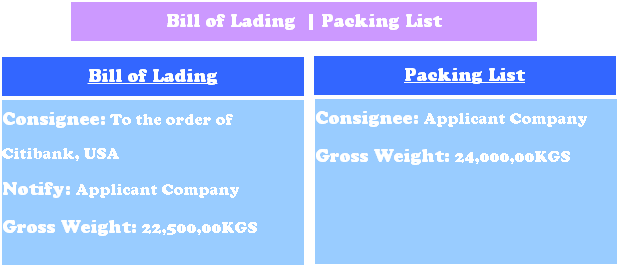

The beneficiary presented a bill of lading and a packing list among other documents with the following data:

Discrepancy Example: Bill of Lading and Packing List Details

Discrepancy: Gross weight on the bill of lading and packing list is inconsistent.

Reason for Discrepancy: Data in a document, when read in context with the credit, the document itself and international standard banking practice, need not be identical to, but must not conflict with, data in that document, any other stipulated document or the credit.

Documentary credits often include a “latest date of shipment”. Latest date of shipment is one of the most important definitions in commercial documentary credits.

As a beneficiary, if you are obligated to make a shipment under a commercial letter of credit, and need to present a transport document; such as a port-to-port marine bill of lading, then you must complete the shipment before the latest date of shipment stated in the credit.

Which means that, the date of shipment indicated on the bill of lading must not show a date, that is after the latest date of shipment marked in the credit.

If you fail to complete your shipment before the allowed time frame, then you will get a late shipment discrepancy from the issuing bank.

After the issuing bank determines that your presentation is not complying, you can reach to the payment only after applicant accepts the discrepancies

Sample Late Shipment Discrepancy under a Letter Of Credit:

A letter of credit has been issued in SWIFT format, subject to UCP latest version, with the following details:

Letter of Credit Conditions

Field 44C: Latest Date of Shipment: 141031

Field 44E: Port of Loading/Airport of Departure: Port of Ningbo, China

Field 44F: Port of Discharge/Airport of Destination: Port of Auckland, New Zealand

Field 46A: Documents Required: Full set of original bill of lading clean on board established to the order of Societe Generale Algerie Spa notify applicant marked freight prepaid.

The beneficiary presented a bill of lading with the following data:

Bill of Lading

Port of Loading: Port of Ningbo, China

Port of Discharge: Port of Auckland, New Zealand

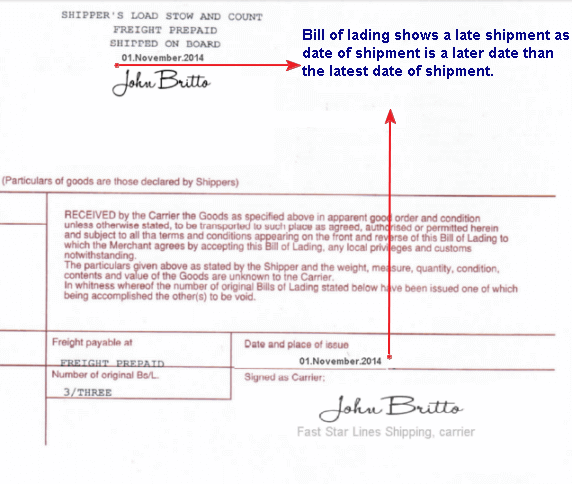

Bill of Lading: The bill of lading is dated 01.November.2014. In addition, it contains an on-board notation as follows: “Shipped on board : 01.November.2014”.

Discrepancy: Marine bill of lading shows a late shipment. Both bill of lading date and on board notation date indicate a late shipment. Date of shipment falls outside the allowed shipment period.

Reason for Discrepancy: If the letter of credit requires a presentation one of the transport documents as indicated in UCP 600, the date of shipment stated on the transport document must not be showing a later date than the latest date of shipment stated in the letter of credit.

Bill of lading shows a late shipment as date of shipment is a later date than the latest date of shipment indicated in the letter of credit.

A bill of lading is a generic term for a transport document, that covers transport by sea from a port of loading to a port of discharge.

Port of discharge can be defined as a port, where a vessel will unload its cargo, from where the cargo will be dispatched further to their final consignees.

Port of discharge, as stated by the letter of credit, should appear in the port of discharge field within a bill of lading.

If the issuing bank finds out that a port to port shipment ends in a different port of discharge than what is indicated in the letter of credit, then the issuing bank will raise a discrepancy, which is known as port of discharge different than letter of credit discrepancy.

Sample Port of Discharge Different Than Letter of Credit Discrepancy under a Letter of Credit:

A letter of credit has been issued in SWIFT format, subject to UCP latest version, with the following details:

Letter of Credit Conditions

Field 44E: Port of Loading/Airport of Departure: Port of Marseille, France

Field 44F: Port of Discharge/Airport of Destination: Port of Incheon, South Korea

Field 46A: Documents Required: Full set of marine bills of lading marked shipped on board issued or endorsed to the order of Kookmin Bank showing freight prepaid, notify applicant and showing the following details: Full applicant name, address as indicated in field 50.

The beneficiary presented a bill of lading with the following data:

Bill of Lading

Port of Loading: Port of Marseille, France

Port of Discharge: Port of Ulsan, South Korea

Discrepancy: Marine bill of lading shows a port of discharge different than what is stated in the letter of credit. Port of discharge should have been Port of Incheon, South Korea, but it was stated as Port of Ulsan, South Korea, which is not as per letter of credit conditions.

Reason for Discrepancy: A bill of lading is to indicate the port of discharge stated in the credit. The named port of discharge, as required by the credit, should appear in the port of discharge field on a bill of lading.

A bill of lading is a generic term for a transport document, that covers transport by sea from a port of loading to a port of discharge.

All shipments, that covered under a bill of lading, must be made between the port of loading and port of discharge, which are stated in the letter of credit.

If the issuing bank finds out that the shipment is effected from a different port of loading than what is stated in the letter of credit, then the issuing bank will raise a discrepancy, which is known as port of loading different than letter of credit discrepancy.

Sample Port of Loading Different Than Letter of Credit Discrepancy under a Letter Of Credit:

A letter of credit has been issued in SWIFT format, subject to UCPURR latest version, with the following details:

Letter of Credit Conditions

Field 44E: Port of Loading/Airport of Departure:

Port of Haifa, Israel

Field 44F: Port of Discharge/Airport of Destination:

Port of Toronto, Canada

Field 46A: Documents Required: Full set of marine bills of lading marked shipped on board issued or endorsed to the order of Royal Bank of Canada showing freight payable at destination and notify applicant and showing the following details: Full applicant name, address as indicated in field 50.

The beneficiary has presented the bill of lading with the following data:

Bill of Lading

Port of Loading: Port of Ashdod, Israel

Port of Discharge: Port of Toronto, Canada

Discrepancy: Marine bill of lading shows a port of loading different than what is stated in the letter of credit. Port of loading should have been Port of Haifa, Israel but it was stated as Port of Ashdod, Israel which is not as per letter of credit conditions.

Reason for Discrepancy: A bill of lading is to indicate the port of loading stated in the credit. The named port of loading, as required by the credit, should appear in the port of loading field on a bill of lading.

The issuing bank or the confirming bank must pay the credit amount to the beneficiary, when they determine that the presentation is complying.

The complying presentation means is that the presentation with zero discrepancies.

If, the issuing bank or the confirming finds at least one discrepancy, then the presentation becomes discrepant.

Under a discrepant presentation, the beneficiary can get the payment, only if the applicant accepts the discrepant documents.

On this post, I am going to explain discrepancies in letters of credit.

Firstly, I will make the definition. Secondly, I will disclose links for discrepancies for each document type. At later stages of the post, I will discuss how to deal with the letter of credit, in order to make discrepancy free presentations.

Definition: Discrepancy can be defined as an error or defect, according to the issuing bank, in the presented documents compared with the documentary credit, the UCP 600 rules or other documents that have been presented under the same letter of credit.

Perhaps, discrepancy is one of the most complicated and “blurred” field in all letters of credit terminology.

The advising bank checks the documents and finds the presentation complying, then dispatches the documents to the issuing bank.

This time, the issuing bank checks the same documents and comes back with a swift message, mentioning couple of discrepancies.

How Could This Have Been Possible?

How could one bank finds multiple discrepancies in a set of documents, while the same documents are found to be complying by another bank.

Alleged Discrepancies and ICC Opinions:

Almost all of the ICC opinions issued so far are related to complaints about “alleged discrepancies”.

What we can see from the results of the ICC opinions is that ICC Banking Committee does not agree with banks in most cases.

Definition or Lack of Definition:

It is strange, but there is no definition of a discrepancy in the letter of credit rules.

Is it too simple to be forgotten? Or too complicated to define? What is the definition of a discrepancy according the UCP 600 rules?

Inconsistency in Application:

Discrepancies varies from country to country, bank to bank, even more; document checker to document checker.

Let me give you a real life example here.

Couple of years ago, I have presented documents to a confirming bank. The presentation has been made under a set of letters of credit, which contain 10-15 pcs of independent letters of credit.

All of these small amount independent letters of credit have the same text and having the same conditions.

Description of goods, port of loading, port of discharge, additional conditions all were the same.

Just, the latest date of shipment and expiry date were changing form one lc to another.

First 3 presentations were found to be complying by the confirming bank. But on the 4th presentation, we received a swift message “MT 734 Advice of a Refusal” indicating a discrepancy on the certificate of origin.

Lessons learned.

Discrepancies can be changed from country to country, bank to bank, document checker to document checker and presentation to presentation.

and here are the results:

According to ICC Trade Finance Surveys, on average, %70 of letter of credit presentations are found to be discrepant on first presentation.

This is a very frustrating outcome, and has a huge negative impact on everyone in letter of credit business.

Why Banks Find too much Discrepancies on the Documents:

Letter of credit rules are often find to be very complicated and hard to understand by exporters and importers.

Most of the small and medium scale export and import companies do not have enough resources to hire a letter of credit specialist in their organizations.

Exporters and importers do not give enough respect to letter of credit rules and standard banking practices. Exporters and importers think that, they can handle letters of credit with ease on their way. However, the fact is different. Letters of credit have very strict rules to follow.

Exporters do not allocate enough time to understand the letter of credit text, before starting to production and shipment.

Some banks open overdetailed letters of credit. Sometimes we see that banks demand almost impossible conditions from the beneficiaries on their letters of credit texts.

Some banks issue foggy (not clear) letters of credit.

Some banks examine documents not as per UCP 600 and ISBP 745.

What can be Done to Prevent Discrepant Presentations:

Pre – Document Preparation Stage:

Keep Your Relationship with Your Customer Close: Please keep in mind that, whatever preventive steps you may take, it is highly likely that you will be facing a discrepancy on one of the documents, that you have submitted. So, it would be very wise for you to keep your relations close with your customer.

Learn the Rules: Before entering a letter of credit transaction, you need to learn the letter of credit rules very well. You should buy one original copy of current letter of credit rules book, UCP 600. Please follow this link to buy a UCP 600 online.

Learn the International International Standard Banking Practices: Before entering a letter of credit transaction, you also need to be familiarized with the International Standard Banking Practices. In order to do that, you should buy one original copy of current International Standard Banking Practices book. Please follow this link to learn more about International Standard Banking Practices.

Check the Credit: You must check the letter of credit as early as you can, before starting to the production. As one of the letter of credit expert indicated “you can not solve lc problems at the presentation stage.” The earlier you are starting to work on the letter of credit text, the better it would be.

Demand a Draft Letter of Credit: Demanding a letter of credit draft from your customer, before having the original letter of credit issued, would be a wise move. This will save you from additional letter of credit fees; such as amendment fees and amendment advising fees.Work on this letter of credit draft carefully.

Check Field 46-A: Check required documents field one by one. Make sure that, you can supply all the required documents, that has been requested under this field.

Check Field 47-A: Check additional conditions field one by one. Make sure that, conditions stated in this field are doable, and are not going to create any problems for you on the presentation stage.

Demand Amendment: If you find a condition or clause that you can not comply with, get in touch with your buyer to amend the letter of credit.

Demand Clarification: If you can not understand a condition or sentence on the letter of credit text, then you should get in touch with the issuing bank for clarification.

Document Preparation Stage:

Complete the documents as requested by the credit. Make sure that, you also take into account the letter of credit rules and international standard banking practices when preparing the documents.

Make sure that, signatures, authentication are made by requested persons or institutions.

Make sure that, you will be presented all required documents without any absence.

Make sure that, you presented correct number of originals and copies as requested by the credit.

Make sure that, the dates on the documents are in accordance with the dates mentioned on the credit. For example, you would not be making either a late shipment or a late presentation.

Make sure that, you will collect all requested documents by the credit as soon as you make the shipment. Once you collect all the documents, you need to make the presentation without losing any time.

After Presentation Stage :

Follow the situation of the documents day by day with the advising bank. Give necessary information to your buyer. And stay in alert mode, until you receive your payment.

No matter how many advantages letters of credit have, they have one big disadvantage. They are expensive.

As a result, you should understand your costs before finalizing a letter of credit deal.

Letter of credit is a secure payment method in foreign trade. But this comfort of security comes with a price.

Letters of credit are one of the most expensive international payment methods available on the market.

As a result, exporters find themselves in a dilemma, when negotiating the terms of the business conditions.

Question is simple but not easy to answer; either choosing an expensive but relatively secure payment method or choosing a risky but less expensive payment method.

What are the Main Letter of Credit Fees That Exporters Have to Pay?

It is really hard to answer this question. Because what rules say is different than what the daily practice dictates.

According to the Rules: The issuing bank must pay all banking commissions as per UCP 600, which is the latest ICC rules of documentary credits.

Real Life Situations: The applicant pays the letter of credit issuance charges, but all other l/c costs will be collected from the beneficiary.

Bank Commissions That Exporters Normally Have to Pay:

Courier Fee / Postage Fee

Advising Fee

Discrepancy Fee

Handling Fee / Negotiation Fee

Amendment Commission

Confirmation Fee

Reimbursing Bank Charges

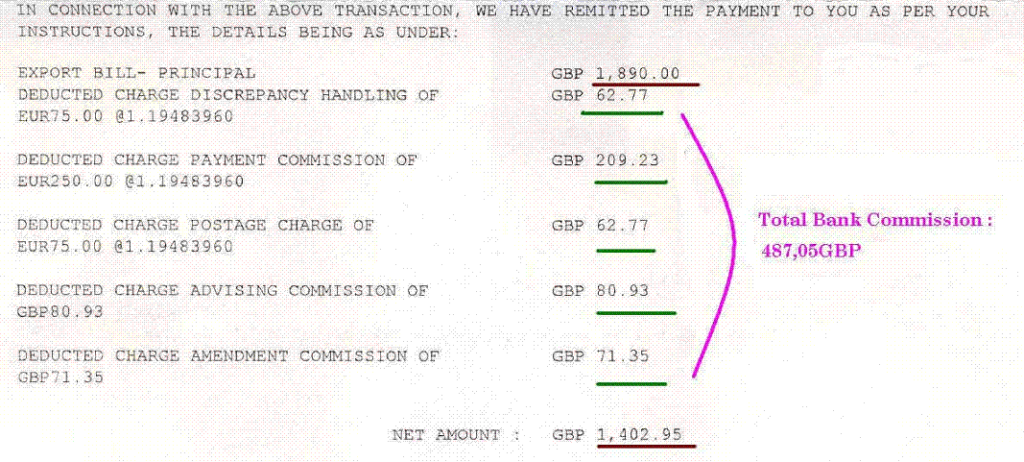

Real Life Example :

I would like to share a real life bank commissions example below.

These bank fees were collected from a British exporter under a letter of credit transaction. As you can see, the exporter had to pay 487 GBP to the banks as letter of credit fees.

Total transaction amount was only 1890 GBP. Letter of credit fees comprised 25% of all transaction amount, and this is unacceptable.

Figure 1 : Real life example of bank commissions under a letter of credit transaction.

Suggestions to Eliminate High Banking Commissions Under Letters of Credit Transactions for Exporters:

Suggestion 1: Do not use letters of credit in low value transactions. As a general rule of thumb, transaction amounts below 10.000 USD to 15.000 USD can be considered as a low value businesses. Try to use alternative payment methods, instead of letters of credit on these occasions.

Suggestion 2: Try to convince your customer, so that the letter of credit fees will be paid by the applicant. Remember, letter of credit rules are on your side.

Suggestion 3: The worst case scenario may be is that, you can not find an alternative payment option and your customer does not want to pay letter of credit charges, except for the l/c issuance costs. If this is the situation, then try to learn approximate bank commissions and make sure that you have included at least some of them on your price offer.

Discrepancy can be defined as an error or defect, according to the issuing bank, in the presented documents compared with the documentary credit, the UCP 600 rules or other documents that have been presented under the same letter of credit.

Discrepancy fee occurs, only when the issuing bank determines that the presentation is not complying.

Issuing banks try to justify discrepancy fee, based on their claim that discrepant documents increase handling costs of issuing banks.

Many trade professionals find these claims unjustified.

Later on this post, you can find the history of the discrepancy fee and how it evolved since its introduction to trade finance word.

But, first of all, I need to explain the usage of the discrepancy fee in letters of credit.

How to Determine, How Much You Have to Pay Due to a Discrepancy Fee, If You Make a Non-Complying Presentation:

Issuing banks must insert discrepancy fee clauses to letters of credit, otherwise they can not demand such fees from beneficiaries.

For this reason, at the first stage, you have to determine, whether or not the letter of credit contains a discrepancy fee clause.

In order to that, you must look at Field 47-A : Additional Conditions.

Discrepancy fee clauses vary from one letter of credit to another in terms of wording. But their structure remains similar. After reading couple of examples, you will be familiarized with them.

Examples of Discrepancy Fees:

Discrepancy Fee Format 1: Any set of documents containing discrepancies and presented to us under this documentary credit, will be charged with a fee of USD 50.00 plus telex charge (if any) at final payment. This charge is for account of beneficiary and will be deducted from any proceeds to be paid.

Discrepancy Fee Format 2: Discrepancy fee for USD 75.- (or equivalent in l/c currency) plus all relative swift/tlx charges will be deducted from documents value for each presentation of discrepant documents under this credit, notwithstanding any instructions to the contrary.

Discrepancy Fee Format 3: If documents are presented with discrepancies and accepted by applicant a fee at the rate of USD 225.

History of the Discrepancy Fees

“As I recall, it all began sometime in the mid-1980s, when banks in US began charging a discrepancy fee – usually about US$25. Over the last decade, this practice spread through the documentary credit world so much that now practically most banks, including some large international banks, engage in this practice. A senior trade finance department manager says: “Now more than 60% of the credits impose discrepancy fees and these credits come from all over the world.” writes Abdul Latiff Abdul Rahim in his article which was published in year 1997 at DCInsight. We have reached 2014 and now almost every letter of credit issued with very little exception contains a discrepancy fee.

Discrepancy fees applied to vast majority of the letters of credit because banks can increase their letter of credit commissions significantly with these kinds of charges.

“Nonetheless, there is a worrying trend whereby more and more items and with higher rates of banking charges are being deducted by banks in the course of L/C transactions. Some of these charges include: opening charges, amendment fees, advising fees, negotiation fees, confirmation fees, transferring fees, reimbursing fees, payment commissions, telex/SWIFT commissions, courier charges, document checking fees, handling charges, discrepancy fees, and commission in lieu of exchange and so on.” Wang Shanlun states in his article published in 2010 at DCInsight.

Unless exporters and importers object these high banking charges in letter of credit transactions, we should expect to see the trend keep going which results higher and higher L/C fees that will be imposing by the banks.

Who Should Pay Discrepancy Fees?

Discrepancy fees are collected from the beneficiaries.

and HAWB (House Air Waybill)?")