Issuing banks often require an ocean bill of lading or a marine bill of lading under letters of credit as a transport document.

The question is whether the title of the bill of lading is important or not when checking the documents?

Letter of Credit Examples:

Ocean Bill of Lading Example

Full set of clean shipped on board ocean bills of lading drawn or endorsed to the order of issuing bank ltd, Sana’a Yemen showing freight prepaid and marked notify

a.applicant (giving full name and address).

b.issuing bank ltd Sana’a Republic of Yemen.

Marine Bill of Lading Example

Full set of clean on board marine bill(s) of lading issued or endorsed to the order of Issuing Bank PLC, notify applicant showing freight prepaid and showing full name and address of the shipping company agent or his representative in Bahrain.

Each shipping line has a pre-printed form of bills of lading.

Some shipping lines are using ocean bills of lading and others are using marine bill(s) of lading.

It is highly likely to be working with a shipping company who has a marine bill(s) of lading pre-printed form where credit calls for an ocean bill of lading or vice versa.

According to latest letter of credit rules

“A bill of lading need not be titled “marine bill of lading”, “ocean bill of lading”, “port‐to‐port bill of lading” or words of similar effect even when the credit so names the required document.”

As a result title of the bill of lading is not important when checking the documents under the letter of credit transactions.

Majority of the letters of credits are asking for a bill of lading which must be issued made out to the order of the issuing bank.

This condition indicated under field “46A – Documents Required” for the letters of credit that are issued in a swift format.

In simple words bills of lading can be classified under two groups: Negotiable bills of lading and non-negotiable bill of lading. Non-negotiable bills of lading also known as sea waybills.

Negotiable bills of lading can also be classified under two main groups. Negotiable bills of lading and straight bills of lading.

Negotiable Bills of Lading: Negotiable bills of lading are the ones that have been issued “to order” or “to order of a named party”. If bill of lading has been issued in a negotiable form, then the buyer of the goods need to surrender at least one original bill of lading to the carrier at the port of discharge. In this scenario bill of lading must be endorsed properly.

Straight Bills of Lading: Straight bills of lading are the ones that have been issued in a way to consigned a named party. If bill of lading is issued in a non-negotiable form, then the buyer can get the goods either by,

surrendering at least one original bill of lading to the carrier at the port of discharge or

in accordance with rules of the national law at the port of discharge which may accept the delivery of the goods to the buyer against proof of identity.

Both “to order” and “to order of a named party” statements make a bill of lading a negotiable bill of lading.

Letter of Credit Examples:

Example of to order and blank endorsed bill of lading: Full set signed clean on board ocean bills of lading made out to order and blank endorsed marked ‘freight prepaid’ and notify Import Bank of India indicating letter of credit number.

Example of made out to order of bill of lading: Full set of original clean on board bill of lading issued to the order of Arab Bank PLC Algeria notify applicant marked freight prepaid.

If a letter of credit indicates that costs additional to freight are not acceptable, a transport document is not to indicate that costs additional to the freight have been or will be incurred.

If you are working with CIF, CFR, CIP, CPT trade terms under letters of credit you are likely to see a statement under field “47A: Additional Conditions” such as “Costs additional to freight is prohibited.”

The logic behind these kinds of statements is to fix the freight cost by the issuing banks to the value that was indicated in the credit.

Normally letter of credit rules allow additional costs which may be shown on the transport documents such as multimodal transport documents or bills of lading.

However issuing banks frequently disallow charges additional to freight by inserting a statement in the credits on this effect, when the trade term is CFR, CIF, CIP or CPT.

Remember on FOB, FCA and EXW terms freight is payable at destination, so you should not be having any problem arising from prohibition of costs additional to freight.

You need to look at the letter of credit text on DAT, DAP and DDP trade terms to determine whether costs additional to freight is prohibited or not.

Examples: 47A: Additional Conditions:

Transport document bearing reference by stamp or otherwise costs additional to freight is prohibited.

Costs additional to freight are prohibited.

Costs additional to freight are not allowed.

Which Costs Can be Regarded as Costs Additional to Freight?

by the use of trade terms which refer to costs associated with the loading or unloading of goods, such as, but not limited to,

Free In (FI),

Free Out (FO),

Free In and Out (FIO) and

Free In and Out Stowed (FIOS).

What Happens If a Letter of Credit Prohibits Costs Additional to Freight?

According to the International Standard Banking Practice if a credit indicates that costs additional to freight are not acceptable, a transport document is not to indicate that costs additional to the freight have been or will be incurred.

Commercial invoice is one of the key documents in a letter of credit transaction.

Almost all documentary credits, either commercial or standby, requesting a commercial invoice from the beneficiaries.

On this article I would like to highlight 5 most common commercial invoice mistakes.

1Description Of Goods On The Commercial Invoice Does Not Correspond With The Letter of Credit:

This is one of the most frequently seen discrepancies on commercial invoices.

According to the latest letters of credit rules the description of the goods, services or performance in a commercial invoice must correspond with that appearing in the credit.

As a result beneficiaries must be very careful when completing the description of goods on commercial invoices.

Example of a Description of Goods Discrepancy: Letter of credit: 45A: Description of Goods &/or Services

Crushing plant. As per proforma invoice no. :P-111-7 R02 dated 03/07/2012 CFR, Bahrain.

Commercial Invoice

Second Hand Crushing Plant. As per proforma invoice No.: P-111-7 R02 dated 03/07/2012 CFR, Bahrain.

Reason for Discrepancy: Description in the commercial invoice would represent a change in nature, classification or category of the goods.

2Commercial Invoice Does Not Show Trade Terms (Incoterms):

When importers and exporters mutually agreed on international trade terms (Incoterms) by stipulating them in a letter of credit, they are bound by these international trade terms as a material part of the contract.

This means that if letter of credit stipulates international trade term under the description of goods section, exporters have to mention this trade term on the commercial invoice as indicated in the credit.

Example of a Trade Term Discrepancy: Letter of Credit: 45A: Description of Goods &/or Services

420 pcs. of black tires size 275/70R225TL148/145J (152e) MC85 model 2011 as per pro. Inv. No. 011 dated 9/6/2011 FOB: Rotterdam Port – Netherlands Incoterms 2010

Commercial Invoice

420 pcs. of black tires size 275/70R225TL148/145J (152e) MC85 model 2011 as per pro. Inv. No. 011 dated 9/6/2011 FOB: Rotterdam Port – Netherlands Incoterms 2000

Reason for Discrepancy: Incoterms not mentioned correctly. Letter of credit stipulates FOB: Rotterdam Port – Netherlands Incoterms 2010 whereas commercial invoice indicates the trade term as FOB: Rotterdam Port – Netherlands Incoterms 2000.

3Commercial Invoice Indicates Goods Which Are Not Mentioned In The Letter Of Credit:

An invoice is not to indicate goods, services or performance not called for in the credit.

This applies even when the invoice includes additional quantities of goods, services or performance as required by the credit or samples and advertising material and are stated to be free of charge.

Example of a Commercial Invoice Indicates Goods Which are not Mentioned in the Letter of Credit Discrepancy: Letter of Credit: 45A: Description of Goods &/or Services

Power Transformer offload 1 Unit Onan 3phs Cu/cu Dyn11 50hz

Commercial Invoice

Power Transformer offload 1 Unit Onan 3phs Cu/cu Dyn11 50hz

Transformer Spare Parts (Free of Charge)

Reason for Discrepancy: Transformer Spare Parts are not called in the letter of credit. Mentioning these goods on the commercial invoice even if free of charge creates a discrepancy.

4Proforma Invoice Presented Instead of a Commercial Invoice:

When a credit requires presentation of an “invoice” without further description, this will be satisfied by the presentation of any type of invoice (commercial invoice, customs invoice, tax invoice, final invoice, consular invoice, etc.).

However, an invoice is not to be identified as “provisional”, “pro‐forma” or the like.

Exporters should not present a proforma invoice instead of a commercial invoice.

5Quantity of Goods Not Consistent With Other Documents:

Any total quantity of goods and their weights or measurements shown on the invoice is not to conflict with the same data appearing on other documents.

What are the risks of a document which is to be issued, signed or countersigned by the applicant in a letter of credit transaction?

In some occasions importers would like to divide letter of credit payments into two or three parts in order to make sure that they will be receiving ordered goods in proper condition.

Mixed payments is used extensively in bigger projects such as capital machinery sales, construction plant installations etc.

On the below example I will be demonstrating a possible scenario as follows:

An exporter and importer have signed a sale contract which is stating that the payment will be done by an irrevocable letter of credit for 100% of the contract amount.

90% of letter of credit amount will be paid at sight against complying shipping documents.

10% of letter of credit value will be paid after the importer accepts the quality of goods by presentation of the installation certificate which is issued and signed by the authorized officers of the importer.

Letters of credit issued with similar conditions as stated above may bring some uncertainties to the exporters, mainly because of the fact that they may not be able to secure their balance payment, which is payable after the acceptance of the goods by the importers.

Exporters may find these clauses confusing and risky. They may want to know what would be their risks under these kinds of letters of credit?

In order to answer this question properly once again we should check ICC’s view.

ICC banking commission explains their stance in this regard at the latest version of the International Standard Banking Practices publication which is known as ISBP 745.

ISBP 745 states that “a credit or any amendment thereto should not require presentation of a document that is to be issued, signed or countersigned by the applicant.”

On the above example 10% of the balance payment requires presentation of a document issued and signed by the applicant, which is openly against the ICC’s stance.

Beneficiaries should remove such clauses from the letters of credit via amendments. If they fail to do so, they may increase their non-payment risk of the balanced payment.

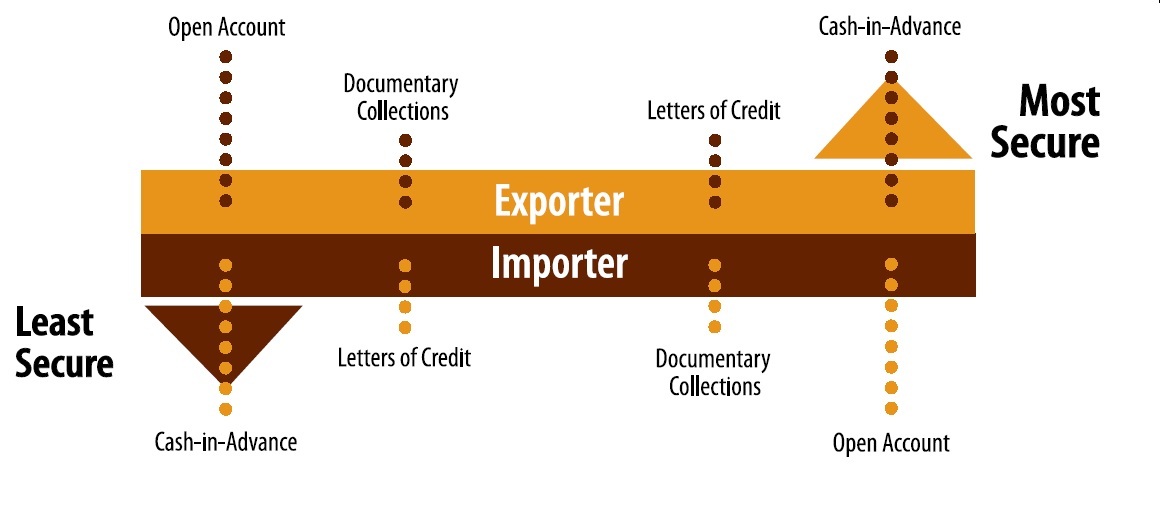

There are 5 types of payment methods available in international trade.

These payment types are cash-in-advance, open account, documentary collections, documentary credits (letters of credit) and bank payment obligation.

Short Descriptions of International Payment Methods:

Cash-in-Advance: Cash in advance is a payment method in international trade in which an order is not processed until full payment is received by the supplier in advance.

Sometimes cash in advance is called cash with order.

Please always keep in mind that under the cash in advance payment, the funds received by the exporters before the ownership of the goods is transferred to the importers.

Cash in advance posses highest risk to the importer, lowest risk to the exporter.

Open Account: Open account means that buyers pay the cost of the goods after goods have been shipped by the supplier.

In an international trade transaction open account defines as a sale where the goods are shipped and/or delivered before payment is due, which is usually in 30 or 60 days.

Open account posses highest risk to the exporter, lowest risk to the importer.

Documentary Collections: International trade procedure in which a bank in the importer’s country acts on behalf of an exporter for collecting and remitting payment for a shipment.

The exporter presents the shipping and collection documents to his or her bank (in own country) which sends them to its correspondent bank in the importer’s country.

The foreign bank (called the presenting bank) hands over shipping and title documents (required for taking delivery of the shipment) to the importer in exchange for

cash payment (in case of ‘documents against payment‘ instructions) or

a firm commitment to pay on a fixed date (in case of ‘documents against acceptance‘ instructions).

A documentary collection (D/C) is a transaction whereby the exporter entrusts the collection of a payment to the remitting bank (exporter’s bank), which sends documents to a collecting bank (importer’s bank), along with instructions for payment.

Funds are received from the importer and remitted to the exporter through the banks involved in the collection in exchange for those documents.

Documentary Credits: Documentary credits, also known as letters of credit, are one of the payment methods in international trade.

Letter of credit defined by International Chamber of Commerce publication of UCP 600 as “any arrangement, however named or described, that is irrevocable and thereby constitutes a definite undertaking of the issuing bank to honour a complying presentation.”

Bank Payment Obligation: Bank payment obligation is a new payment method in international trade.

Bank payment obligation (BPO) is an irrevocable undertaking given by an Obligor Bank (typically buyer’s bank) to a Recipient Bank (usually seller’s bank) to pay a specified amount on a agreed date under the condition of successful electronic matching of data according to an industry-wide set of rules adopted by ICC.

What are the Key Points of Consideration When Choosing an International Payment Method?

Financial Needs of the Parties: Open account payment term is a credit granted by the exporter in favor of the importer. In contrast, cash in advance is a credit granted by the importer in favor of the exporter.

Letters of credit available by deferred payment and documentary collections payable with time drafts are also financial credits supplied to the buyers.

For these reasons financial needs of the parties is a key element determining the payment terms in international trade transactions.

Negotiation Power of the Parties: Sometimes exporters are in pressure to sell their products. On the other hand, importers are desperate to find a particular good in a short period of time.

If balance of the trade power diminishes in favor of one party, then the stronger party may want to benefited from the situation and dictates most favorable payments terms.

Country Risk of the Exporter and the Importer: As an example if the importer residents in a developed country whereas the exporter sits in a risky country, then the importer may do not want to take risks and choose the most secure payment method for himself.

Sector of the Transaction Parties: Occupying sector of the exporter and the importer is one of the most influencing element that effects the determination of the payment method. For example, food and textile sector practicing open account payments or documentary collections, on contrary oil sector uses letters of credit.

Willingness to Take Risks of the Parties: Willingness to take risks is one of the key factor determining the payment method in international trade.

Occasionally exporters want to take extra risk, while importers tend to trust their suppliers.

A risk taking exporter may ship the goods against open account terms whereas a risk taking importer may decide to pay in advance.

If both parties want to limit their risks, then they should either choose documentary collections or documentary credits.

Legal Legislation: If you want to export to Algeria, you have to choose either documentary collections or letters of credit as a payment method. This is an Algerian legislation and every exporter that makes business with Algeria has to obey this rule.

“At the beginning of August 2009, the Algerian government released the ‘Complementary Finance Law 2009’ which decreed that all imports into the country, with a value exceeding $1000, would require a documentary letter of credit (LC)”

Country Practices: Middle East countries tend to use letters of credit intensely, when importing goods. Chinese exporters also use letters of credit in great volumes. USA importers using documentary collections for small value purchases. German importers would like to pay 30 days after bill of lading date under open account payment terms.

Pre-shipment inspection, PSI, is a part of supply chain management and an important and reliable quality control method for checking goods’ quality while clients buy from the suppliers.

Main objective objective of the inspection certificate is to satisfy the importer or the

government body that the goods are in conformity with the indicated specifications

on the sales contract or proforma invoice.

Inspections are important tools to reduce trade risks and avoid fraud.

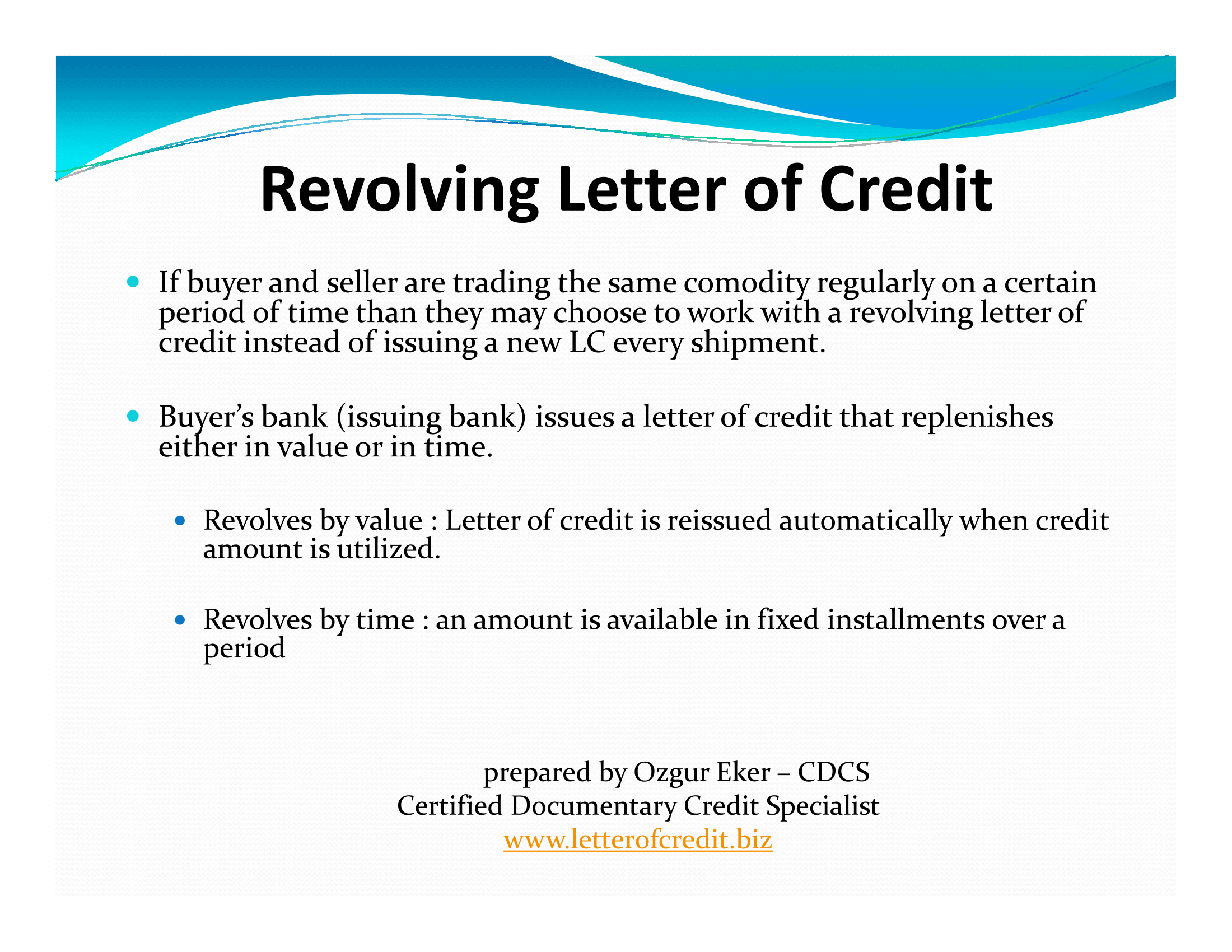

If buyer and seller are trading the same commodity regularly on a certain period of time than they may choose to work with a revolving letter of credit instead of issuing a new LC every shipment.

Buyer’s bank (issuing bank) issues a letter of credit that replenishes either in value or in time.

Revolves by value : Letter of credit is reissued automatically when credit amount is utilized.

Revolves by time : an amount is available in fixed installments over a period

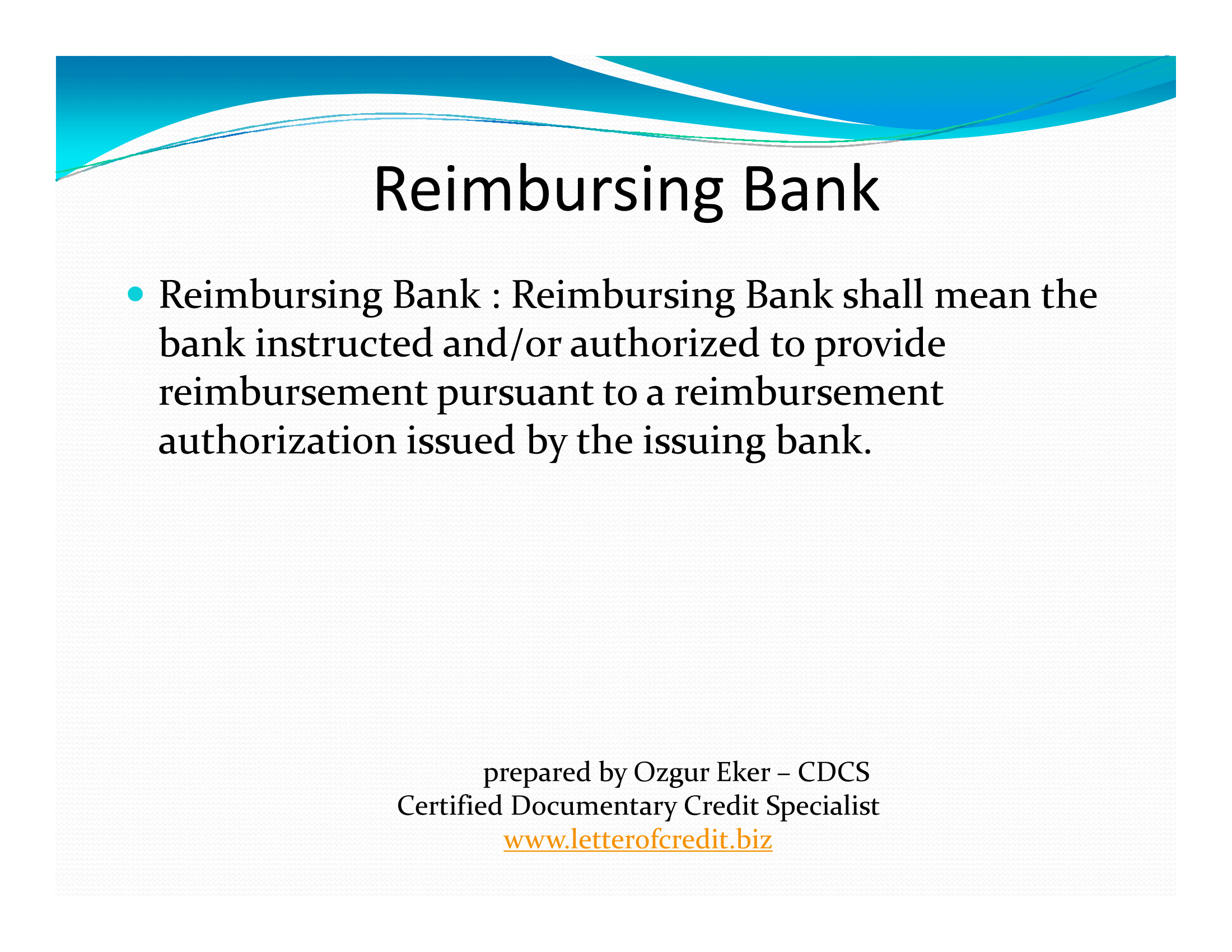

Reimbursing Bank : Reimbursing Bank shall mean the bank instructed and/or authorized to provide reimbursement pursuant to a reimbursement authorization issued by the issuing bank.

and HAWB (House Air Waybill)?")